When it comes to picking CCW insurance, the options can be a little overwhelming.

Just like any other type of insurance though, it’s always a good idea to check out the offerings of a few companies before deciding on which policy to go with.

Luckily, we’ve gathered the best of the best to help you narrow down the choices and find out which insurance is right for you when you’re carrying a CCW (concealed carry weapon).

Followed up by a quick description of what all the legalese means.

THE QUICK LIST

-

Editor’s Pick CCW Coverage

-

Most Affordable

-

Best Educational Content & Coverage

-

Budget No Limit Plan

-

Mid Tier Plan

Table of Contents

Loading…

How We Chose the Best CCW Insurance

Our team of a practicing attorney, licensed insurance agent, and journalist started this article with a list of all insurance companies on the market that offer concealed carry insurance.

From there, we began digging into specifics like cost, plan, and extra features like access to training or online learning opportunities. Each insurance company was then assigned a rating based on benefits and coverage.

We then ranked the insurance plans and compiled them into our list here. For comparison on each company’s specific rating for each category, scroll down to the Comparison Charts section below.

CCW Insurance Comparison Charts & Analysis

The five insurance companies we looked at were rated side-by-side on cost, plan, and perks.

Cost

Each plan offers its own pricing and the chart below is a look at what each base level plan costs at a monthly and annual level.

| Company | Cost (Monthly) | Cost (Annually) |

| Second Call Defense | $14.95 | $179 |

| Right to Bear Insurance | $17 | $185 |

| CCW Safe | $19 | $209 |

| US & TX Law Shield | $24.95 | $299 |

| USCCA Membership | $29 | $299 |

Plan

Though we evaluated each company’s base-level plan, several of the companies we reviewed offered more than one plan, allowing users to tailor coverage to their needs. Below is a list of each company’s total plan offerings for personal coverage.

| Company | Total Number of Plans Offered |

| Second Call Defense | 3 (Defender, Ultimate, Ultimate Plus) |

| Right to Bear Insurance | 1 (3 optional add-ons with extra fees) |

| CCW Safe | 7 (Ultimate, Defender, HR-218, Protector, Freedom, Constitutional Carry, Home Defense) |

| US & TX Law Shield | 6 (Defend, Defend + Civil Liability, Discover, Explore, Navigate, EmergencyShield) |

| USCCA Membership | 3 Membership Levels (Gold, Platinum, Elite) |

Perks

Perks include additional benefits like access to e-learning or in-person training opportunities and extra coverage like red flag coverage or lost wages that are included in the base plan. Note: this is not comprehensive, just a short list of benefits we think are useful.

| Company | Additional Benefits |

| Second Call Defense | Gun retrieval or replacement, 24/7 emergency legal hotline, education and training, local attorney referral in 24 hours |

| Right to Bear Insurance | 24-hour emergency hotline, Training and educational content, Discount to industry partners, Gun replacement, 40 counseling sessions |

| CCW Safe | Access to 24-hour hotline, Red Flag Law coverage up to $5K, Firearm replacement (if applicable), Up to 10 licensed professional counseling sessions, Crime scene cleanup |

| US & TX Law Shield | Red Flag Coverage, Bystander Coverage, and Accidental Discharge Coverage |

| USCCA Membership | Universal gun cleaning kit, interactive online training and educational content, USCCA qualifications with online + in-person training Level 1, Concealed Carry Magazine archive for 1 year |

Mulit-State Coverage

| Company | Additional Benefits |

| Second Call Defense | Membership not available to residents of NJ, NY, and WA, or U.S. territories. |

| Right to Bear Insurance | Coverage in all 50 states with multi-state add-on for $4.35 per year |

| CCW Safe | Coverage not available in NJ, NY, and WA. |

| US & TX Law Shield | Coverage in all 50 states, Washington, D.C., and Puerto Rico for Home + Carry Explore and Navigate Plans. |

| USCCA Membership | Coverage not available to NJ, NY, and WA. |

Important Coverage Types

Civil…criminal…what? These legal terms you’ll see below can be downright confusing. Here’s a quick overview of what they mean and why you want to be protected.

Civil Defense

Concealed carry insurance offers protection against liability claims resulting from using a firearm for self-defense in a civil claim. Some plans also protect against using any other legal object.

We also cover if plans offer coverage upfront or merely reimburse (not good).

It can cover things such as:

- attorney fees

- bail bonds

- lost wages

Criminal Defense

Even if the shoot was good, you’ll possibly still be charged with a crime.

If you don’t want to go to jail you’ll probably want a criminal defense attorney specializing in firearm self-defense. Most of the plans allow you to select your own so you aren’t stuck with the lowest bidder.

Bail Bonds

Bail comes up several times and it’s an agreement to show up in court for a certain amount of money.

Bail bondsmen typically charge 10% of the bond upfront for their service, and this is what most plans cover. Example: if you have a $1,000,000 bond, the plan will cover the required $100,000.

Best Concealed Carry Insurance

Worth noting before we start that all of these options focus on the lowest tier of pricing. Many of these companies offer multiple plans, so if these don’t cover what you want, consider upgrading to a higher-level plan.

1. CCW Safe – Editor’s Pick CCW Coverage

Prices accurate at time of writing

Prices accurate at time of writing

-

25% off all OAKLEY products - OAKLEY25

Copied! Visit Merchant

Pros

- No limit criminal & civil defense costs

- Covered self-defense use of force

- No claw-back policy

- Up front payment

Cons

- Some plans require a CCW license

- Some plans don't have civil liability

CCW Safe is a well-established and time-tested CCW coverage plan.

One of the biggest draws for CCW Safe is that there is NO LIMIT on the amount of criminal or civil defense.

Plus, you don’t have to worry about getting dropped from coverage as long as you are in a covered location where you have “admissible evidence” of self-defense or the self-defense of others.

Put this together with no reimbursement even if you’re found guilty and you’ve got a winning combo.

As for payments, CCW Safe has up front payment for defense (because who has a couple hundred grand to drop) as well as $750 to $1000 daily to offset your loss of income depending on the plan.

Coverage Details:

The most popular Defender plan that does require a valid CCW license:

- States Covered: Coverage not available in NJ, NY, and WA.

- Monthly Cost: $19 (Annual Cost: $209)

- Civil Defense Coverage Limit: No limit

- Criminal Defense Coverage Limit: No limit

- Bail Amount: $1,000,000

- Lost Wages Compensation: Up to $750/day

- Additional Benefits: Access to 24-hour hotline, Red Flag Law coverage up to $5K, Firearm replacement (if applicable), Up to 10 licensed professional counseling sessions, Crime scene cleanup

Yup…we have a full review of CCW Safe too that covers all the other plans…such as ones for retired MIL/LEO, Constitutional Carry states, or home coverage only.

2. Right to Bear – Most Affordable

Prices accurate at time of writing

Prices accurate at time of writing

-

25% off all OAKLEY products - OAKLEY25

Copied! Visit Merchant

Pros

- Most affordable coverage

- Unlimited defense expense coverage

- No claw-back if you're found guilty

Cons

- Additional services sold separately

If you like options and some flexibility, Right to Bear presents a decent option for those looking to be insured.

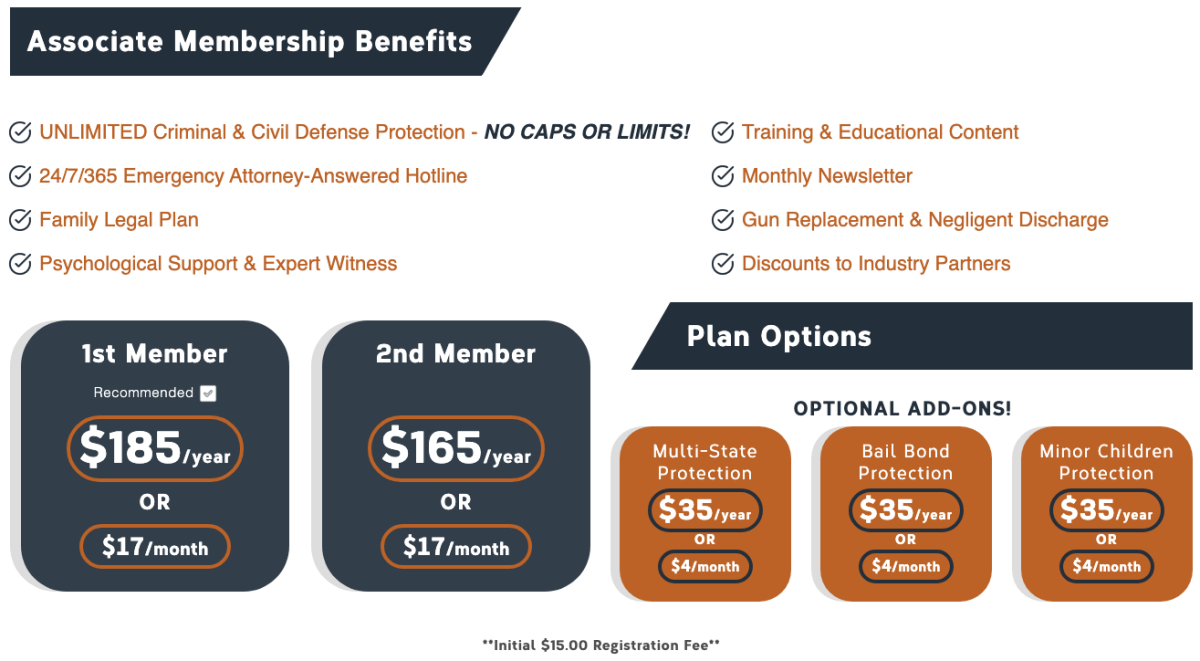

Offering a single budget-friendly tier at only $17 a month or $185 a year, Right to Bear makes a CCW self-protection plan achievable.

And…use code PEWPEW15 to knock it down to $158/year.

They’ve also upgraded their plan to be unlimited for both civil and criminal court. And if you’re found guilty in criminal court, they won’t claw back the amount.

They also have some other great features, such as online training, psychological support, expert witness coverage, and industry discounts.

And something that I just found out and isn’t on their Features list (but is on their Education tab) is that they’ll replace your gun if it is taken after a self-defense incident.

However, if you’re looking for extras like spousal insurance, bail-bond coverage, minor coverage, or multi-stage coverage, those are add-ons.

And something new this year is their family plan for $380 or $35/month for 2 adults and unlimited minors. It’s hidden a little bit but you can find it here when you sign up:

Coverage Details:

- States Covered: Coverage in all 50 states with multi-state add-on for $4.35 per year

- Monthly Cost: $17 (Annual Cost: $185)

- Criminal Defense Protection: No limit

- Civil Defense Protection: No limit

- Additional Associate Coverage: $17/month ($165/Year)

- Multi-State Coverage: $4/Month ($35/Year)

- Bail Bond Coverage: (Up to $100,000) $35/Year

- Minor Household Children: $4/Month ($35/Year)

- Additional Benefits: 24-hour emergency hotline, Training and educational content, Discount to industry partners, Gun replacement, 40 counseling sessions

See our full review of Right To Bear here, and don’t forget PEWPEW15 for 15% off.

3. USCCA – Best Educational Content & Coverage

-

25% off all OAKLEY products - OAKLEY25

Copied! Visit Merchant

Pros

- Lots of educational content

- $2 million liability insurance limit

- No limit for defense expenses

- Freebies when you sign up

Cons

- Price increases

- Not available in all states

One of our team’s favorite option isn’t technically insurance.

However, they are the biggest player whenever someone thinks about “concealed carry insurance.”

But rather, it is a membership where you get tons of education and have personal liability insurance a part of your membership.

A little confusing…but I go over it ALL in my USCCA review. And if it helps…I’ve been a member since 2017!

I’ll go over what tier to get, a breakdown of all the courses you get, and how to get a free course from Pew Pew Tactical as well.

They had a big update in June of 2024, which increased their bond expenses, added red flag coverage, and clarified plea deal coverage plus recoupment.

Coverage Details

- States Covered: Coverage not available to NJ, NY, and WA.

- Monthly Cost: $39 (Annual Cost: $399)

- Liability Insurance Limit: $2,000,000 annual aggregate

- Defense Expense: No Limit

- Cost of Bail Expenses: $250,000 of funds. A $2,500,000 bond usually costs $250,000 or 10% of the total.

- Incidental Expenses: $20,000

- Red Flag Coverage: Up to $15,000 in attorney fees and expenses

- Actual Loss of Earnings: Up to $10,000

- Additional Benefits of Membership: Universal gun cleaning kit, interactive online training and educational content, USCCA qualifications with online + in-person training Level 1, Concealed Carry Magazine archive for 1 year

Will USCCA Drop You If You’re Convicted of a Crime?

There was a lot of fear that USCCA would drop you quickly if you were convicted of a crime. So now they added that if you take a plea deal that doesn’t involve a “crime of violence” you’re ok.

Examples include murder, aggravated assault, kidnapping, arson, robbery, extortion, and unlawful possession of a firearm.

Impartial Coverage Determination

Before, it was up to the insurance company to determine whether what you did was self-defense.

Now, the insurance company is required to grant you coverage if the judge allows the argument to be made in court and your attorney believes there’s a good-faith self-defense claim.

Plus, coverage will continue until there’s a final non-appealable finding of guilt.

USCCA In-Person Training

USCCA has tons of instructors all over with their most popular course being the Concealed Carry and Home Defense Fundamentals.

I recently had the chance to take their AR-15 Fundamentals class which was phenomenal and geared towards beginners, however the Pew Pew Tactical team still learned a bunch!

Plus…new signups with our link get a free access code to our video Beginner Handgun course.

Get the rest of the details here.

What’s your take on the USCCA?

4. US & TX Law Shield – Budget No Limit Plan

Prices accurate at time of writing

Prices accurate at time of writing

-

25% off all OAKLEY products - OAKLEY25

Copied! Visit Merchant

Pros

- No limit for criminal or civil defense

- Up-front payment

Cons

- No bail coverage at the basic level

- No lost wages compensation at the basic level

US & TX Law Shield offers a relatively competitive plan, at very competitive prices.

With that lower price comes some tradeoffs.

You’d think a smaller company with lower prices wouldn’t be able to compete with the big boys at all. And you’d be wrong. Despite their size, US & TX Law Shield actually has no limit on their civil or criminal defense coverage.

What’s more, the payments are made upfront, so you don’t need to worry about waiting for reimbursements on attorneys’ fees while you’re busy planning your legal defense.

The lower cost has to be made up somewhere, right?

With the cheaper offering from US & TX Law Shield, their basic plan offers NO lost wages compensation, and there are additional charges tacked on to the plan if you want to have bail coverage or have your policy effective throughout the entire US.

It’s essentially a way to tailor your plan to suit your needs. Though after adding back in all the coverage offered as part of a standard policy by the other companies, you might end up paying about the same anyway.

Coverage Details:

- States Covered: Coverage in all 50 states, Washington, D.C., and Puerto Rico for Home + Carry Explore and Navigate Plans.

- Monthly Cost: $24.95/mo

- Civil Defense Coverage Limit: No limit

- Criminal Defense Coverage Limit: No limit

- Bail Amount: No coverage at the basic level

- Lost Wages Compensation: No coverage at the basic level

- Additional Benefits: Red Flag Coverage, Bystander Coverage, and Accidental Discharge Coverage

5. Second Call Defense – Mid-Tier Plan

Prices accurate at time of writing

Prices accurate at time of writing

-

25% off all OAKLEY products - OAKLEY25

Copied! Visit Merchant

Pros

- Up-front payment

Cons

- Lower coverage limits

Second Call Defense sits right in the middle, offering decent coverage limits. They aren’t the best, but also not the worst.

Like some of the better plans, Second Call Defense offers upfront payments of all your covered fees, such as attorneys’ fees. So, you don’t have to shell out the money yourself for bail or during the trial.

The coverage also ranks right up there with the big boys and covers the entire US in their standard plan.

As a middle-tier offering, the criminal defense coverage is on the lower end, as is the bail amount. Of course, this is pretty much expected going in.

Coverage Details:

- States Covered: Membership not available to residents of NJ, NY, and WA, or U.S. territories.

- Monthly Cost: $14.95/mo

- Additional Spouse Coverage: $5/month

- Civil Defense Coverage Limit: Unlimited

- Criminal Defense Coverage Limit: Unlimited

- Bail Amount: Up to $1,000,000

- Accidental Shooting Protection: $50,000

- Additional Benefits: Gun retrieval or replacement, 24/7 emergency legal hotline, education and training, local attorney referral in 24 hours.

How to Choose the Best CCW Insurance For You

This is where you get the favorite answer of lawyers everywhere…it depends.

While it seems like a cop-out, it really does depend on what you want, and what you think you’ll need.

Even the staff here at Pew Pew Tactical have gone with different providers to suit our individual needs, ranging from USCCA to Right to Bear and CCW Safe.

The main thing is that you get some type of insurance, rather than none at all.

Ultimately, just like choosing any other insurance policy, try to see which of these plans seem like they would fit you the best, and check them out in detail.

We even have a couple of reviews on some of the providers, to help you make a more informed decision – if you haven’t read those, take a look at our USCCA and CCW Safe reviews.

Even at around $20/mo for a typical CCW insurance policy, the money adds up, and could easily be spent on ammo instead, so it’s a good idea to be sure you know what you are getting for your money.

Everyone’s situation is different, and someone in a free state like Texas may want to consider a policy that provides more coverage than someone living in the heart of New York City.

It’s also important to note that not all the policies we compared are available in all states. There are varying insurance and firearms regulations across the 50 states, so it never hurts to pick a few options just in case your top choice isn’t available in your home state.

Why Trust Pew Pew Tactical

This article builds upon research conducted by licensed and practicing attorney and Pew Pew Tactical contributor Paul Yen who went through the plan contracts and chose the top performers.

Editing and adding to the article is Pew Pew Tactical CEO and Founder Eric Hung. Eric is a licensed insurance intermediary in 48 states (sorry, New Jersey and New York) who cross-compared the different insurance liabilities and educational content of each plan.

He’s also an NRA-certified pistol instructor and a USPSA/3-Gun/NRL22 competitor. Eric has also researched and written over 250 articles on firearms and gear.

Editor-in-Chief Jacki Billings runs our experienced team of reviewers. She is a member of the Society of Professional Journalists, ACES: Society for Editing, and the Professional Outdoor Media Association. Jacki has a bachelor’s degree in journalism and has worked as a media professional for close to 20 years, specializing in gun media for almost 10 years.

She uses her professional journalism and editing experience to set testing protocols and editorial standards for Pew Pew Tactical.

FAQs

How much does concealed carry insurance cost?

Concealed carry insurance is between $11 to $49 a month depending on provider and tier.

Does concealed carry insurance cover lawsuits and attorney fees.

Most will cover civil and criminal defense costs as well as bail, damages, and lost wages.

What is concealed carry insurance?

It's a type of coverage that provides legal protection if you use a firearm or other weapon in a defensive situation.

Final Thoughts

While everyone’s got their own views on insurance policies, at the very least, consider coverage limits and bail amounts when shopping around.

At the end of the day, it all comes down to your situation and what works best for you. But, again, any insurance plan is better than none at all.

Was there a CCW Insurance that we didn’t cover? What CCW insurance did you choose? Let us know in the comments! If you’re looking for a new CCW gun, take a look at the Best CCW Guns!

CA #4272012

LATEST UPDATES

- June 2025: Added state coverage

- May 2025: Expanded on CCW Safe details and shifts in rankings.

- September 2024: Expanded on how we tested and evaluated each insurance company.

- July 2024: Added additional information to USCCA and CCW Safe.

{kind=link}

170 Leave a Reply

Thanks Sean for getting back with me. I know you will not be disappointed with FLP.

As far as I know, you have never included FLP, Firearms Legal Protection. FLP provides fantastic unlimited coverage for both criminal and civil protection. It is less than $10/month. The biggest benefit with FLP is there is no pot of gold for an attorney to go after so the chances of having to deal with a civil lawsuit would be extremely rare. As far as I know, they have not yet had to deal with a civil lawsuit. Please do all gun owners a favor and include FLP in your next update.

Thank you Lyle, we'll keep them in mind!

Look into Attorneys on Retainer (AOR). They cover all 50 states.

Ok, so I live in New York State. USCCA does not insure in this state.

SO... where is the list for U.S. States these companies "don't" cover. this should be in the description of these companies under "cons" don't you think? otherwise your readership has to go through each and every one of them on their own. Please try to be a bit more thorough in your articles!

Thanks for the suggestion, David. We'll definitely keep that in mind when we update this article next.

I did not see attorneys on retainer here Why !??

Simple answer Lawrence, we haven't had any experience with them. In most cases, we try to write about things we've tried.

I did not see attorneys on retainer here why??

Washington State has insurance agency restrictions, and unfortunately concealed carry and self defense insurance aren’t allowed. I found this out when I inquired into USCCA. Washington State has been Democrat controlled for TOO LONG.

Did you come up with any other options Jerry?

They cover you if you have a permit or live in a constitutional carry state. Otherwise there is a home only plan for those who live in states where it is difficult to get a permit. AKA where it’s legal.

And if you’re in Washington state, you’re out of luck.

Is this also not true for USCCA?

You lose a lot of credibility when you do not proof your copy for grammar.

"If your lawyer's pants look like this, you going to jail"

Where TF did your writer go to grammar school at?

It's a meme...we didn't write it. It came like that.

I was also with USCCA at one time, but as others have mentioned, after finding out a few odd things on their coverage and non-caverage, never went back with them, Went CCW safe , like their coverage much better.

Yes, current AOR member, Ex USCCA member. AOR has FEW in any exclusions.

Former USAA member, dropped coverage due to terms of coverage in certain circumstances are either vague or a deal breaker. First -no coverage if incident occurs in an area of restricted use -gun free zones & involving the use of alcohol...Disclaimer for exiting eatery after 1 or 2 .drinks with the meal -too easy for a NO coverage incident. The alcohol denial is too vague. I am in favor denials for intox incidents but denials for minimal usage.

I presume the author is also under a marketing contract with USCCA and cannot speak the truth like others are now that they are away from the contract.

as long as you are not deemed to have committed a crime (whether you did or not), otherwise you are paying $hundreds for training that is largely free elsewhere on the internet.

Yes, I'd like to hear your comments one these people.

Thank you.

I was with uscca for over 7 years, but for several reasons I dropped them last year and went with CCW Safe.

USCCA:

I joined at the highest level because at the time it was the highest amount of legal coverage. The next year they dropped the lowest plan and added one higher than mine. Back door price increase as most will take the best coverage. Shortly after that they made all the plans have the same legal coverage and the only difference was how many training videos you could get to. I like most of their content, but the same stuff is widely available online for free. Then they kept substantially raising the cost, and right now they have a notice on their site it’s going up another $120 per year in all their plans next month (feb 2025). When they declined to defend multiple paying members, that was it for me. When you buy car insurance and you get in an accident that is your fault, the insurance company still has to cover you and they can’t deny coverage or recoup their payout. Even guilty have the right to a defense attorney and like your car insurance company USCCA is paid by many members into a pool by s majority of people who will never make a claim.

Have you looked at Attorneys on Retainer by chance? Thank you!

I was a USCCA Elite member for 10 years and dropped them September 2023 after all the adverse publicity in not covering two of their members. My wife and I have CCW Safe (Ultimate Plan) and very happy with it. I think USCCA has great training and education and I liked their magazines that go out 8x a year. I picked USCCA back up in January 2024 as a secondary provider so I could get their training education and magazine resources. With that said, I think CCW Safe has the better and more comprehensive coverage but I think they lack in the training and education area which is where USCCA has the edge. I don't mind having coverage in both places as each provider has what I need and desire.

With all the crap that came out about USCCA policies and ability to support you if you were charged with a crime (they cannot help you in that case because they are insurance, not lawyers) and the fact that they outright dropped support for paid members who had legit need for help with a self-defense situation... you rate them #1? I think you recycled old material that was written before all that info came to light and now you're just filling the marketing campaign funnel with useless and potentially misleading recommendations. I don't trust them and now you're suspect as well for promoting what is likely a very bad choice for peace of mind - when you really need it, you are going to regret choosing USCCA (IMHO). Lawyers can defend you under any circumstance. If your local police decide to charge you with a crime, insurance cannot legally do anything for you... so your money is gone. Make the decision based on how well you know your local police or sheriff (in much of the country, I would not take the risk).

Can you have coverage by more than one company at a time for the different benefits?

Please review Armed Citizens Legal Defense Network, Inc

Is there anything legal to buy in New York?

US Lawshield has changed their new memberships. It would be interesting to see a more up to date review regarding them.

That's not very comforting.

If you're a veteran, you and your spouse will get full CCW Safe coverage for $25 per month - that includes unlimited legal fees for a criminal and a civil trial. The only thing you won't get is, if you lose a civil case (a lawsuit), they won't pay the claim. It will cost about $40 mor per month for that coverage.

I had written the following, in the above post:

There was a lot of fear that USCCA would drop you quickly if you’re convicted of a crime. So now they added that if you take a plea deal that doesn’t involve a “crime of violence” you’re ok.

That's not very comforting...

The first paragraph didn't make it into the post, for some reason.

Yes I was curious of your thoughts of Attorneys for Freedom / Attorneys on Retainer as well.

Attorneys for Freedom have a plan. Though, technically, not insurance.. it's like always having a lawyer on retainer. Was wondering if anyone has tried these guys.

I agree and have asked the same question but received no answers. I am thinking along the line of an attorney "on retainer" without all the classes in info USCCA offers. Don't get me wrong, I have USCCA and always have however, with funds getting tight, I have been looking for the primary reason only right now. And that is a lawyer and insurance. I can get the insurance so now I am working on the lawyer.

The U.S. LawShield rate just went up to over $400 per year

That depends on the coverage you choose. We pay just over 300 per year for the two of us for the lowest plan but with multi state coverage added. We may have a discount for being retired military though that I've forgotten.

I see no mention of Armed Citizen's Defense Network.

Established 2008.

Thanks for the review. Offering two comments for your next update.

Notably, CCW Safe offers a substantial discount for active or retired military or law enforcement officers, honorably discharged military veterans, and other credentialed first responders including firefighters, EMTs and paramedics.

And, as noted by T.N. below, in October, Right to Carry has increased their premiums and no longer falls in the "Most Affordable" category.

Thanks for the heads up!

I know it's not insurance but how do you feel about the Attorneys on Retainer group?

Just an FYI, Right to Bear basic plan is $15 a month, not $11.

Google Kayla Giles

You mention claw bar in some reviews, but not USCCA. Does USCCA have a claw back stipulation if you're found guilty?

Yes it does

I just called USCCA which I have been a member since 2017 and they told me that they do not have claw back! which I believe in this sad day of woke people on our juries. this is something we really should have!

If you get charged after all the appeals you will have to pay them back, that's what the lady at uscca said to me. I was a member for a year

No

I know some plans do not cover charges from negligent discharge, and some do. I'd like to know which ones do.

I just talked with US Law Shield today and their upper level plan has the accidental discharge coverage.

See for example: YouTube video

"Did you know that USCCA dropped Alan Colie? Check out the full video analysis on our channel!"

And others have been dropped too... even before going to trial.... or mid legal representation....

Anyone reading this should know by now that that is false. Alan Colie was not dropped. He used his option to not use USCCA. He even wrote an email to the president of USCCA to settle the rumors. You can do a YouTube video search and find this out.

Any info on Firearms Legal Protection?

I bought a policy for their plan at a seminar I attended last year which is up for renewal now.

Bob

USCCA may be the biggest because they constantly flood you with ads. At least they used to - I haven't seen their ads in a while. Whenever a company floods me with advertisements, I tend to think that there isn't much substance behind all the ads.

I chose CCW Safe when I found out that Don West was their National Trial Counsel -- he was George Zimmerman's lawyer in the Trayvon Martin case. My thought is that if he was able to get George Zimmerman declared not guilty in that case, I want his team of lawyers to defend me should I ever be charged. In other words, I want the very best legal service if I am ever charged for using my handgun.

The use of 'Concealed Carry Insurance' is incorrect. Its actually liability insurance that provides coverage if you conceal carry or not plus its not limited to just defensive gun use but rather will cover you no matter what you use in a legal defensive situations unless specifically limited in the coverage. So check the policy coverage to make sure, and that it covers nationwide.

A little explanation about USCCA.

Although the USCCA entity its self is not an insurance, a benefit of membership with USCCA is being covered under the Liability Insurance Policy (AKA 'Self Defense Insurance') Issued to the United States Concealed Carry Association (USCCA) by Universal Fire & Casualty Insurance Company.

The policy covers you for any form of legal defense and it can be with hands, guns, knives, running them over with your car, anything you use for legal defense in a situation that requires it. Your family members can also be covered.

This is NOT fully accurate... it has been reported.... that USCCA has dropped a number of cases before a case ever goes to trial. Also if found guilty or if a case in pleaded you may have to repay all legal expenses back to USCCA.....

What about Armed Citizens' Legal Defense Network? Is there a reason they did not make the list?

Armed Citizens' Legal Defense Network is not an insurance nor does it offer insurance as a membership benefit by a policy issued to them.

Armed Citizens' Legal Defense Network is a pre-paid legal service. Basically its keeping a lawyer on retainer to defend you and that's it. The cost expenditures in a complicated case may exceed what the board is willing to approve, I think their limit is $25,000.00 before board approval for more is needed.

Unfortunately, most of these “policies” have more holes than a piece of Swiss cheese …all of which can easily result in a denial of coverage. They almost never cover unintentional discharges (the single most common gun-related incident that results in legal charges), they often don’t cover incidents related to family members or people you invite into your home, they may not cover you if you have imbibed any alcohol or are on prescription meds, they generally don’t cover you if you use a firearm in self-defense related to a vicious animal attack (again, a common scenario) and worst of all, they generally deny coverage if a self-defense shooting takes place where you were not legally supposed to carry a firearm (in some states these “gun free zones” change on what seems to be a daily basis). In at least one state that I am aware of, you cannot carry on ANY private property whatsoever without the express permission of the property owner, and many states ban concealed carry on any public transportation, public parks, etc.

Carl, really great points. Do you have CCW “insurance” and, if so, which offering did you choose?

Thanks.

Robert

uscca is scam shame for you having them on here

US LawShield is not "the smallest." They started as the first prepaid legal company in 2009 and are still the largest at over 750,000 members -- as large as USCCA without the magazine and firearms instruction. They cover full scope of work, hands (physical assault), hunters, negligent discharges, appeals, any criminal charge where defense can be articulated, and have no caps.

USCCA only covers you when compensatory damages are involved--so there is no criminal defense. If you are convicted of any criminal charge, your coverage ends--including if you take a plea. So no appeals (for criminal), and they recoup all the money from you if they paid out anything before you were convicted. They do not cover scope of work (no LEO, etc.). You only get one incident every 12 months, and it can ONLY be when force to stop an imminent threat of grave bodily injury or death is used (no assaults). You also agree to sue on their behalf, and anything you are owed in damages you must give to them. You are paying for a magazine subscription; it is basically useless unless it's a clear-cut in-home shooting where no charges are filed, and damages are available.

Right to Bear (a wing of Palmetto State Armory) does not cover hands--only weapons. They are also not unlimited.. "THE TOTAL, AGGREGATE AND CUMULATIVE LIABILITY OF THE ASSOCIATION, IF ANY, FOR ALL CLAIMS UNDER THIS AGREEMENT OF ANY KIND WHATSOVER, WHETHER IN AN ACTION BASED IN CONTRACT, TORT (INCLUDING NEGLIGENCE OR STRICT LIABILITY) OR ANY OTHER LEGAL THEORY, SHALL NOT EXCEED AT ANY GIVEN TIME THE TOTAL AMOUNTS PAID TO THE ASSOCIATION BY ALL ASSOCIATES HEREUNDER IN THE IMMEDIATELY PRECEDING SIX MONTHS." They only cover (for all members) what they made in the last six months. They have the smallest member base of any company doing "this;" so if you are the next Rittenhouse, they will NOT have the funds to cover you fully. They also do not cover anyone who uses self-defense while working for/in a gun shop, range, or store selling any such devices and ammunition.

Both USCCA and Right to Bear's model is the individual getting into an incident, then trying to find their own attorney who they must hope accepts the terms, and then coverage can begin. This is not the case with US LawShield; your named attorney will answer the phone and (if feasible) show up on the scene immediately to assist. There is no waiting time trying to search for one. They only place in the network each state's best criminal defense attorneys -- for $10.95, 14 years later, they still can't be beaten. Happy to cite any contracts/member agreements if clarity on these coverages is needed.

I like the highlighted best plans for insurance, but additionally we will need an excellent legal team. Do these companies (CCWSafe or USCCA) help find/recommend a legal team, or are you out on your own for that?

CCW Safe will either provide you a lawyer or let you use a lawyer of your own choosing - the choice is entirely up to you. That's another thing I like about CCW Safe.

Just FYI. New York has BANNED NRA insurance. To make it even more risky to own a firearm in NY.

NY TAC Defense

I decided to go with CCW Safe Ultimate. I wanted something that would cover civil damages, since there always seems to be a civil suit following any incident, and CCW Safe has 1M coverage. The cost of the premium is high but I would rather pay now than regret it later. I didn't like that USCCA would not pay if you are found guilty, which would include a guilty plea to a lesser charge.

CCW Safe offers $2 million coverage for the member ($10 per month add-on) and $1.5 million for the spouse ($20 per month add-on) on civil liability (that's what they will pay up to if you are sued and lose).

I just learned about Bluecoat insurance. Coverage seems very good. Any knowledge of the company?

I'm wondering why the Armed Citizens Legal Defense Network wasn't included here. I'm a huge fan, believe it's the best.

I am thinking of going with Armed Citizens legal - does anyone have any experience with them - any thoughts or advice?

My only experience with them is my membership, their coverage which unlike some companies do cover both criminal and civil cases, and appeals, and do not demand repayment if you lose. Bail benefit caps 50k I believe.

To me their coverage/benefits are straight forward and their website does a good job of providing info. I do recommend thoroughly reading coverage detail, you know the super long fine print some people skip.

Many companies seemed to have many "if, then, but" clauses and were more convoluted, USCAA comes to mind. USCAA does tout their large focus on training; however, as you know one can learn only so much from watching vids.

Armed Citizens Legal Defense Fund sends a few books, has a series of videos, but that's it. I did call to talk to them to get more info before signing up.

I also had prior knowledge of the people who came together to create the company, Mas Ayoob and Jim Fleming in particular.

I'm sure you're familiar with Mas Ayoob. Sadly, Jim Fleming passed away last year. Before becoming a defense attorney, he was a policeman. Shorty before he passed away, he wrote the following exceptional book which if you haven't read it, I highly recommend.

By Jim Fleming: AFTERMATH: Lessons In-Self Defense: What To Expect When the Shooting Stops

I wish you the best luck in finding your preferred company.

It says it in the name. It's a legal team. Not an insurance policy

If you accept a plea deal, say a misdemeanor rather than go to trial, which over 90% of SD cases end up that way, USCCA's insurer will NOT pay one penny. Why? You admittedly committed a criminal act.

CCW Safe dies not cover any incident in which Force is used against other family members ir when Force is used against people who are in member's house with permission or by invitation, excluding servicemen, delivery, contractors, etc.

Since many self-defense incidents involve family member or people known to a defender, this should be a no go for most people.

From CCW Safe:

"No that is not true, we used to have a domestic exclusion in our terms but it has been removed and as long as it is a legal self defense incident we will provide coverage."

Did you have any recommendations about the NRA's option: Lockton Affinity Outdoor’s Personal Firearm Liability Insurance? What about coverage for your spouse? USCCA charges $199 more. Do other providers?

You should have rated Firearms Legal Protection. In looking at plans, they seem to be right there, or better, than what’s compared here. Not complaining. Thanks for what you do!

Yeah, I think it's odd they didn't list FLP...I've looked at everything out there and FLP is the way to go.

FLP only covers you if you use a weapon (no physical force and no pepper spray) and only when there is the threat of grave bodily harm or death (no assaults). They do not cover appeals, scope of work, or negligent discharges. You pay them if you call the emergency number by accident and also have to pay $49.99 just to ask an attorney a question. Not the best choice.

It isn't clear whether "defense coverage" means only paying for attorney fees and costs to defend a criminal or civil case, or an actual civil judgment or settlement. Can that be clarified?

USCCA is NOT what it used to be. The per Diem is higher than everyone else. If you lose or found guilty in any way, regard of on what count or if it is a reduced charge, they will make you pay the money spent from USCCA back. USCCA is technically not insurance. It says it in the paperwork you receive. You are basically prepaying expenses. Most others are actual insurance. There are some other changes I do not like as well but those are the two main reasons why I am switching. Those of you that have had this insurance a long time, please read you policy since it has most likely changed since you purchased it.

I love US Lawshield. I never have had to use them for a case as if yet, but I travel for work and at times for personal pleasure. The nice thing about US Lawshield is you can call them and talk to a attorney and ask questions about gun laws in both your state and any state you may travel through. You can also call and ask about different changes in the laws and what they mean.

Have you reviewed Self Defense Fund? selfdefensefunddotcom

CCW Safe for me. The Defender I do have my ccw permit

You left out Firearm Legal Protection

I just mentioned that too. They seem the best so far to me. Had USCCA for a year until they upped their cost. Compared others and thinking of FLP. They could have a better website though to explain more.

Before buying USCCA Insurance, read the policy, you will discover that it no longer specifies civil defense coverage.

I’ve read a lot of reviews and everyone leaves out a critical element...civil DAMAGES. If you are sued civilly (not criminally) and the person suing you is awarded damages, who’s going to pay for those? Some may thing their homeowners liability insurance but most policies have intentional act exclusions that would give them the right to deny the claim. This is potentially much larger than say per diem costs, which some reviewers emphasize as an important feature.

Going on what Terry said below, if you take a Plea Deal (which nearly any person would) USCCA will DEMAND ALL their money back also. They will pay up ONLY if you are found Not Guilty!!

Uscca if your found guilty in a self defense trial Uscca has it in their police they can demand all their money back leaving you high and dry. Read their police.

Here’s a reality of insurance: you don’t buy insurance because you need it. You buy insurance in case you need it. A good example is the money I spend on health insurance. I’ve always been fairly healthy, and have never generated enough expenses to justify the outlay. Two years ago I was diagnosed with a high grade cancer. Long story short, I think the insurance has paid out so far something close to $1.2 million.

If you find yourself in a situation to use a firearm defensively, and get charged, that insurance to cover the bail will be worth the price of admission for that alone. Add in the attorney fees, lost wages, getting your gun back, getting your life back on track, not bankrupting your family... how much would that be worth to you?

Don’t buy because you heed it. Buy in case you need it.

Well, you didn't discuss Armed Citizens' Legal Defense Network which is 'recognized' by Massad Ayoob, a very well respected firearms (police) instructor. What do you think of the Armed Citizens' Legal Defense Network and Massad Ayoob?

I have had ACLDN membership for 5 or more years, I don't remember how long. They have been an excellent choice from the start. The initial membership includes an extensive DVD and Online training course and recommendations. Marty and Gila are great people to work with and are accessible, unlike the monster CCW insurance companies. I have received some very good manuals and books from Massad Ayoob, free of charge. Knowing he's on their Team is reassuring. He knows more than most people have forgotten. It's time to renew, and do it I will. Recommended highly!

"He knows more than most people have forgotten."

Brilliant. I know not to take advice from Tig.

So, what about Firearms Legal Protection? How do they rate?

I just signed up for US & TX Law Shield. I can add/drop extras (such as 50-state coverage) as needed when I travel out of state.

How was the sign up experience?

Has anybody looked at secondcalldefense.org who also offer a CCW policy. I am considering them now for their middle plan but am unsure of the support for their program ( I seem to se an A rated policy is in the background but no confirmation of their field performance

Do any of these plans offer coverage for a wrongful arrest for concealed carry? For example, what if a local cop doesn’t recognize your LEOSA credentials or he’s of the opinion that your CCW permit from a different State is not valid in their state?

Firearms Legal Protection is one of only a few where you immediately talk to a lawyer and not an answering service. They are on the case right away where as others review the cases once weekly to see what they will take. So say they review them on a Thursday morning and you get arrested Thursday afternoon you will sit in jail for a week and that's hoping they will take the case. I have the Family Premium Membership for $35./month and know a lawyer will be with me quickly and not next week. I also will talk with a lawyer and not an answering service. Whatever you do keep your mouth shut as soon as you call 911. And just say "There has been a Force on Force Firearms Related Incident" Nothing more until you talk your lawyer.

Insurance coverage is useful only if it kicks in if you are arrested and need bail money and an attorney.

When looking at these policies, you have to think of the most unlikely and ridiculous scenario, you could find yourself in and ask if one of these outfits provides coverage.

Here's an example: are you covered if arrested for possession even when you carry lawfully with a CCW and possess a weapon you own legally? The answer, for USCCA, is "NO" because the presumption is if you're not carrying legally, you are already in violation of the law, and they cannot and will not defend you. Yet, if you are involved a self-defense incident (except in N.Y., NJ, and W.A.) in the same jurisdiction, they will defend you.

I'm a USCCA member on the Elite plan ($47 per month). I'm also a retired law enforcement officer authorized to carry concealed in all 50-states and territories of the U.S. by federal law (see LEOSA, 2004).

Federal law supersedes state laws when governance over the same matter arises. But in some anti-gun States like N.J., N.Y., and W.A. (where most of these outfits do not provide coverage), some local jurisdictions pass laws to try to supersede or restrict CCW and LEOSA. In N.J., there are reports of arrests of active and retired LEO's for violation of local ordinances for violations of restrictive ammo ordnances. Yes, you read that correctly. LEO's in N.J. check the type of ammo CCW and LEOSA authorized persons carry and, arrest violators if they carry unauthorized ammo (e,g, hollow points).

The point is, you have to think through what could go wrong when you carry. In this day and age, even the most innocuous situation leading to your arrest could put you in a position where coverage does not kick in even though you may think it should do so. And the whole point of coverage is to ensure you don't have to sell everything you own to pay for your defense.

What happens if you have two CCW insurance plans such as USCCA and CCW Safe. Who pays? and will one cover the difference if say one doesn't have enough to cover all the bail or defense?

USCCA will not cover you if any other entity exists that can be responsible for your case, period. "When this insurance is excess, we will have no duty under this Coverage to defend the “insured” against any "claim" or suit if any other insurer has a duty to defend the “insured” against that "claim" or suit."

CCW Safe will attempt to negotiate and work with other entities if terms are agreeable.

How many of the mentioned plans have the backing or underwriting of a credible insurance company to guarantee the company’s financial credibility and ability to come through when its member needs it? For example, USCCA is self insured. It has no insurance company backing! Depending on USCCA requires its members to rely, solely, on its financial strength to cover them in an emergency. Yet, USCCA refuses to provide its members with any accounting of its financial strength! In other words, the paying member has no assurance that, when he/she needs coverage, that USCCA possesses the financial strength to be there! If a carrier cannot/will not provide its member evidence of its financial credibility, then relying on that company is like buying a “pig in a poke”! Yet, my review of several company plans indicates that USCCA offers the best all-around benefits! It, really, is not an encouraging situation! Maybe the absence of insurance underwriters to such companies is a highly revealing deterrent!

If they are really legit why would they not offer up proof of solvency?

Actually, in the matter of legal coverage if you ever have to shoot your gun, it's better that they are self-funded. The NRA found that out - they provided this type of insurance. Anti-2nd Amendment groups then pressured the insurance company to cancel the insurance; and NRA members were left with nothing.

CCW Safe says that it is a benefit that they are self-funded so that anti-2nd Amendment groups can't pressure get the insurance cancelled. Another reason I decided to go with them.

I’m wondering if I were to get a ccwsafe defender plan for $179 but then supplement it with the ACLDN so I would have my civil liabilities covered for only $135 vs $220 a year with the add on civil coverage as well an advantage in the state of Washington. Any thoughts? Also what about Firerms Legal Protection? I hear no mention of them and from the website they look pretty enticing as well.

The reviews seem to be pretty thorough, however none cite the number of policies they have in force or the number of cases they have defended and/or won for their clients. I'm all for ccw insurance but I think that it's important to know their experience record and how successful they've been in defending their clients. Mentioning George Zimmerman may be good publicity but I wouldn't hang my hat on one case.

Just wanted to say thanks for doing this comparison. It was very helpful and I appreciate your work !

This was helpful. Called my insurance agency thinking my homeowners would have some coverage -- duh. No. I ultimately, after agonizing over it quite a bit going back and forth primarily between USCCA and CCW Safe, went with CCA Safe. Thanks for a great article to get it rolling for me. I hope I NEVER have to find out how good it is!

You did not mention LegalShield which is what Front Sight is recommending and what actually got me looking in to getting some sort of CHL Insurance.

LegalShield makes to pay for their base legal coverage for random stuff (like divorce and car accidents), then you pay to add the gun owner supplement--so it starts at $44.90. They cannot be charged with a crime and be covered by them. You may only call the emergency line once you are detained by police. They do not cover bail. No other coverage can exist. It only covers shootings with firearms--no physical force, discharges, or brandishings. For gun owners, you are capped at 20 hours pre-trial and 40 hours trial. This is worthless for a significant case such as murder--which is why they do not cover criminal charges. They do not cover appeals and do not cover cops/security. For the money, any other option is a better option than them.

Some of the information in this article is wrong. I googled CCW Safe, the article says there is NO limit to the coverage, their website specifically say’s limit is one million dollars. Best to do your own homework, before you buy, I went there to buy it, but didn’t.

Thanks Gary, policies change so we'll double-check and update the article!

Hello!

We reached out to CCW safe to double-check and the coverage remains the same "Criminal, civil and administrative defense costs are covered 100% without cap." The $1mil cap you saw is for damages awarded (if you lose the civil case), not the cost of the defense. The defense is covered 100%.

Thanks for clarifying that, my bad.

Reading comprehension. Invest in it.

Civil liability insurance up to $1 million for $220/year. Legal defense coverage, both criminal & civil, is unlimited.

I am going to start the process to get my CCW here in CA and I will for sure purchase coverage to protect myself in case I ever have to use my weapon to protect my self, but I am stuck deciding between two of the companies above. USCCA & CCW Safe. I am leaning towards CCW Safe because it offers unlimited dollars for criminal defense and civil defense.

As an insurance agent, don't hold that against me, I often tell my clients to buy the most insurance they can afford and that is why I think CCW Safe would be the best option because defense costs can use up the $250,000 max USCCA offers in a blink of an eye leaving me picking up the rest.

What is stopping me from pulling the trigger, is the shear number of people who recommend USSCA, most of which are experts in firearms. So I guess I am asking, for a compelling reason to go with USCCA beyond the amazing amount oftraining materials they provide and/or compelling reason to not go with CCW Safe. HELP!

This may come a bit late to you from the date of your posting, but I just came across it today. I guess we all have to also take in consideration that maybe USCCA pays more for it’s advertising (pays people for recommending USCCA as a great company), just be weary … I did see a YouTube video that discussed that we should read the policy/literature SECTION 1, subsection 1 to see that it really does NOT fully cover you as a paying member.

USCCA WAS UNRESPONSIVE. I emailed them 3x asking them to answer a few Qs before I make my decision to join, and NO ONE EVER GOT BACK TO ME. I even “chatted” with a rep who confirmed the email address was correct. Both CCWSAFE and US LAWSHEILD had comprehensive replies to my questions within 36 hours. Lesson learned: USCCA will take the time to bombard you with marketing emails but cannot spare a few minutes to answer questions for a prospective member.

(Note: Due to disability, I am not able to call; this was not an issue for CCWSafe or US LAWSHEILD —- they were there for me when I needed them.)

Hmmm. If they were that unresponsive during the SALE cycle - I can't even imagine how responsive they would be should there be a case opened. Pass! These folks should respond to Email within 24 hours (business days). I work at a high tech company and get between 200 and 300 Emails daily - now, not every email requires a response, but prospects and clients get my #1 priority and get my attention within 1 hour. 1 day is mediocre in this day and age! So I say, put them to the test (as you have). Nicely done.

What do y’all think of Firearms Legal Protection?

US and TX Law Shield have been the defendant in a class-action lawsuit as of 2015. I don't know how or if that case was resolved, but they apparently had pretty shady contractual practices that allowed them to opt out of representing their members. Of course, that defeats the entire purpose. I'd like to see this review updated to take that into consideration.

I believe they were found not guilty or whatever the word is I’m looking for at 1am when I should be sleeping. :) Just go find out how it was resolved. Also, I’m pretty sure uscca is the one with the sketchiest record between the two. :)

I currently use FLP (Firearms Legal Protection) since it was recommended by SDCGO a few years back. I would be interested in your assessment of them

It appears from their website that CCW Safe has NY, NJ and WA limitations. Otherwise, coverages look very strong.

A few of these insurance companies opt out of covering people in NY, NJ and Washington. Whos next?

What about Legal Shield? Any opinions? They are the endorsed provider by Front Sight (for what it's worth).

I have Legal Shield and I just found out they have supplemental insurance for gun owners, but it looks like it is not as comprehensive as the ones listed above. From what I read they provide you some access to ask questions from attornies that specialize in firearm law, 20 hours of pre-trial and 40 hours of post-trial representation and then discounted rates, which is very similar to their regular Legal Shield plan I have, but it does not provide all the other bells and whistles. So I would call a limited plan and it is $12.95 a month in addition to the regular plan. It is better than nothing, but I think the plans above are better and offer more comprehensive plan. The one thing the Legal Shield plan offers is the assistance of an attorney to file NFA paperwork if that is something you are looking for at $250.

Have you - will you rate FLP - Firearms legal Protection , plz. They say they have coverage in both Civil and Criminal suits, Uncapped Attorney Fees, all 50 states, lost wages reimbursement, firearms confiscation coverage, Bail up to $250K, expert witness/investigator fees, etc.

I wish you had included ACLDN. They have a long and good track record. Their biggest disadvantage compared to CCW Safe and USCCA is a relatively small war chest. For example, I doubt they could have funded George Zimmerman's defense.

Hey Kendahl, ACLDN is definitely on our radar, but like you mentioned, they are relatively small, and so didn't make the cut this time. That being said, some of my friends have used ACLDN to supplement their primary CCW insurance and have been pretty satisfied with that setup.

I use ACLDN to suppliment my membership in another firearms owners' defense company with higher limits. ACLDN is only $95 per year after the first year, and their Advisory Board includes Massad Ayoob, John Farnam, Tom Givens, Dennis Tueller and attorneys James Fleming and Emanual Kapelsoh.

Yeah, I want those guys on my side.

The author of this article states he chose CCW Safe as his insurance provider.

Paul,

Can we discuss the new Lockton Affinity Outdoor Personal Firearm Liability insurance offering?

Hi Jeff, that one didn't make it onto our list this time, since we were only considering the 5 most popular ones, but maybe next time! For what it's worth, I believe Lockton was involved with the now-defunct NRA Carry Guard, so the policies may be similar, especially in terms of reimbursement of legal fees after the charges are dropped or you are acquitted.

Look up the "Best's" rating on Lockton -- you probably will decide to forgo using them.

Has anybody heard about Self Defense Fund (SDF)? It looks good on paper, but there's not as much information about them online as about some of the bigger names.

My LTC instructor was trying to sell us LegalShield in class but I don't like being pressured to buy so I wanted to more research on these companies. Thanks for you article and have you any opinion on or heard about LegalShield LTC insurance?

Hey Daniel, my understanding is LegalShield is a standard insurance that allows for a gun owner's supplemental insurance, so you would not be able to purchase that insurance without an existing LegalShield insurance policy. This article is mainly focused on CCW insurance that is independent of standard insurance policies, but I'll definitely give other offerings another look in the next article!

USCCA offers "Gun Confiscation Without Due Process" protection. Does CCW Safe offer this protection? I did not see anything about this on their site and can not find this issue in comparisons.

Yes, if you opt in for the Ultimate Plan ($499/year in one payment):

"EXTREME RISK PROTECTION ORDER COVERAGE (“Red Flag Law” Coverage): The "Ultimate Plan" is the ONLY membership subscription that covers a legally issued Extreme Risk Protection Order that does not follow a Recognized Self-defense Use of Force Incident. CCW Safe will provide services and a contracted Attorney to represent the Primary Member and the Spouse who are Ultimate Plan members if they are found to be the subject of an Extreme Risk Protection Order. This will include all legal proceedings or hearings. CCW Safe will pay the legal fees of the Contracted Attorney up to the maximum amount of $10,000 per covered member."

(Quoted from https://ccwsafe.com/terms)

They claim to be the only company that offers this benefit.

And no, I do not work for them. I just happened to have been reading through their Terms of Service earlier today. You do you.

I live in NJ and had CCW Safe. I believe they have the best policy out there. However, one day I received a letter basically saying "As of now we are not covering you anymore." Reason given is because of our new governors stance on guns. I can't blame them for that. But leave me suddenly hanging without any coverage is abysmal to say the least. They should have been courteous enough to give me a few days to get other insurance.

So what did you do or what company did you select instead?

Has anyone used 2A-Legal.com ? If so what do you think?

US LawShield is in NJ still.

Tried to sign up with USCAA & quickly discovered Washington state insurance commissioner has fined & barred them from selling insurance in the state. Washington state is fast becoming an anti-gun state suffering from the left-coast cancer spreading northward. Is there any protection for CCW in this state?

Yes, Armed Citizen Legal Defense Network, they are not insurance and they are headquartered in Washington State.

Thank you. I am looking for CCW... something

Good article and review, Paul. I went with the Defender offering from CCW Safe. It was close though as USCCA and Law Shield are comparable. I have a CCW permit in Wisconsin so the plan I chose seemed the best fit for me, combined with the no limit coverages.

Do any of the insurers cover "negligent discharge" situations?

US LawShield does. LegalShield, CCW Safe, and FLP do not. I am not 100% on USCCA, but I would imagine not since they don't even cover criminal charges--I am sure their insurance would not help you with an ND.

US Law Shield also covers appeals and any retrials with no dollar limit!

That is good to know, as I had not even considered that possibility; which in this litigious culture is more likely a probability.

I see you commented 18 minutes ago hopefully you are still on. What about civil insurance? most wont cover it or its a lot more extra. Do I need this? How important is it? Wayne

I notice there is bias in your article.You lean towards USCAA because they have been around the longest. If you compare them to CCW Safe there is no comparison in value.

CCW Safe -Monthly cost – $22/mo

Civil defense coverage limit – no limit......HUGH

Criminal defense coverage limit – no limit.....HUGH

Bail amount – $500,000.......HUGH

Lost wages compensation – $250/day........HUGH

USCAA - Monthly cost – $22/mo

Civil defense coverage limit – $500,000

Criminal defense coverage limit – $100,000

Bail amount – up to $100,000 (amount is deducted from criminal defense limit)

Lost wages compensation- $3000 total

How can you possibly say USCAA is a better plan ??

Have not selected a plan yet. Was leaning towards USCCA until I saw the type of aggressive, intervention training they are doing. Talked to a firearms Attorney and apparently others are troubled also.

Can you explain that a little more..

Not sure why one would discount disqualify Law Shield because of the class action suit against them for over aggressively pushing their service at TX LTC (CHL) classes, when USCCA overaggressively pushes their services in your email inbox every single day.

I have been looking and CCW Safe has the best coverage...

Hi, went with Armed Citizen Legal Defense Fund....hope I don't need it but am glad to have it.

One main reason I may switch from USCCA to TX-LAw shield...

https://www.uslawshield.com/huntershield/index.php?st=tx

I used the link you provided and it seems to only be ads for insurance for hunters.

I do not see where it offers any insight into using TX Law Shield over USCCA or any other carry insurance?

Also, do any of them cover you if you act to save someone else's life?

It's listed under "Good Samaritan" coverage. I did see it somewhere in my all day research so far, but I don't know where. Most STATES have Good Samaritan law exemptions for emergencies such as life saving.

US LawShield covers you criminally and civilly (unlimited) if you perform medical aid after a shooting or similar event, as long as you take their trauma course

What about Firearms Legal Protection?

Uscca will not take clients from WA state, because of insurance regs. Bummer!

Also, same problem as Ryan...can’t see last few columns in chart.

US LawShield is the only company in WA state. They do their due diligence in working with state DOJs to operate there and have retained permission to cover members living in WA.

Cannot read the read the last two columns on the right side of the chart. Ads cut them off. Definitely an interesting topic for me. I would like to see the whole chart.