There’s a TON of choices out there for self-defense learning and insurance.

And like you…I wanted to make sure I had the best.

I feel it’s one of those things that when you really needed it…you want it to be the absolute best.

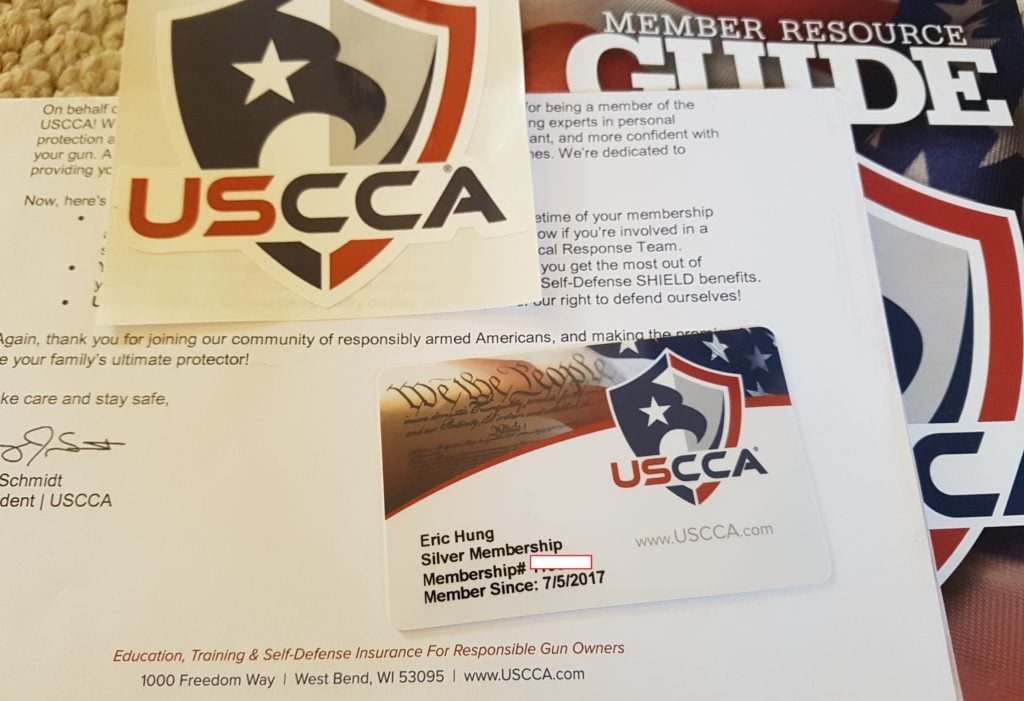

Well…I guess there’s my seal of approval (since 2017)!

Read on to learn more about why I chose USCCA’s membership for both its learning library and added personal insurance benefits* all members get.

2025 Update: I’m an Elite member (with a better camera now). And I added an in-depth review of almost their entire video library, plus the February 2025 policy changes.

Table of Contents

Loading…

Why Trust Me?

I’m Eric Hung, the founder of Pew Pew Tactical, and since 2023 I’ve become a licensed insurance intermediary in 48 states (sorry NY and NJ).

I’ve written hundreds of articles about firearms on Pew Pew Tactical, especially from the beginner’s point of view since that was me not too long ago.

And I carry on a daily basis to protect myself and my family.

I’m bringing that same mindset to this USCCA review with easy-to-understand aspects of their training and coverage.

So you know what you’re getting.

What’s Included in a USCCA Membership?

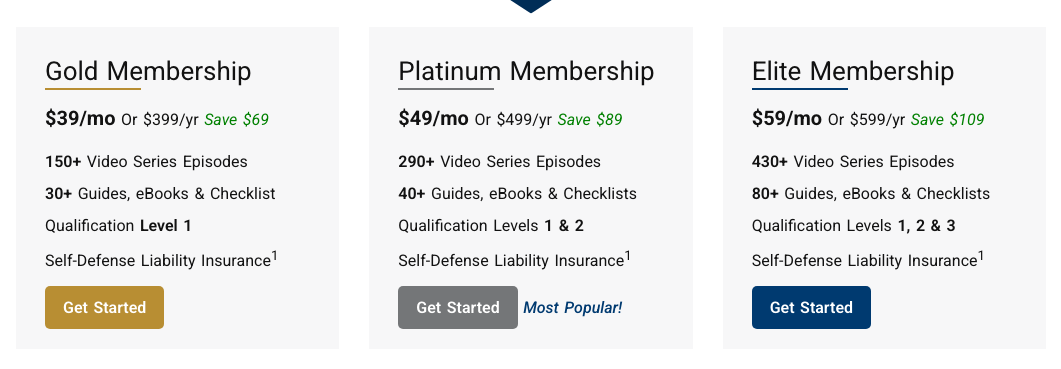

There are currently three tiers of USCCA membership:

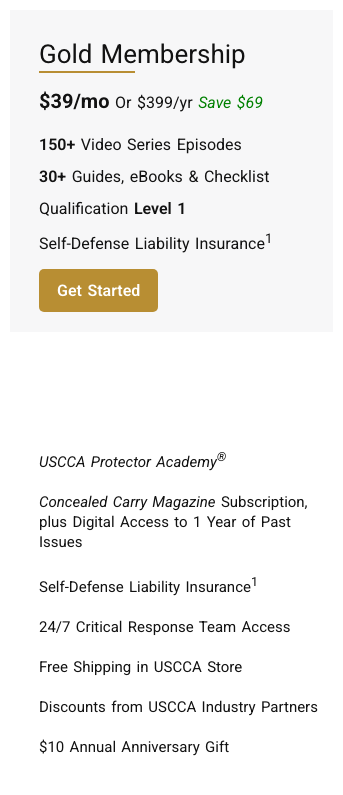

- Gold Membership: $39/month or $399/year (save $69)

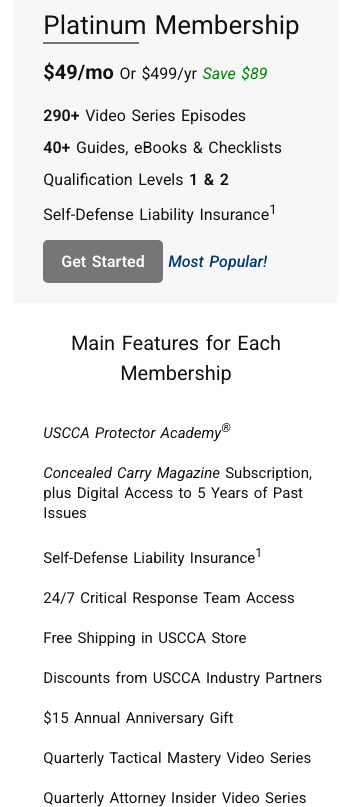

- Platinum Membership: $49/month or $499 a year (save $89)

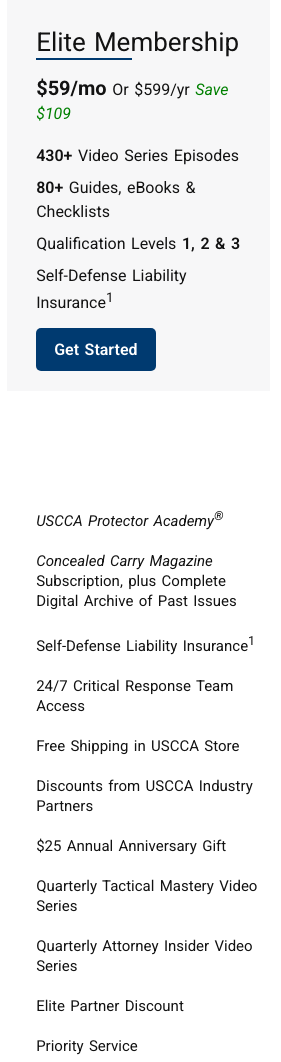

- Elite Membership: $59/month or $599 a year (save $109)

They differ in the amount of education and training content you’re able to access on the USCCA website.

Don’t worry…I’ll go over all the major points and differences between each tier.

What About “Concealed Carry Insurance?”

You probably know USCCA and other competitors for “concealed carry insurance” but it’s a common misnomer that stuck.

All USCCA members become insured on the self-defense liability insurance policy issued to the USCCA*.

And as of October 2021…there are no longer defense expense limits.

Here’s the rest of the good stuff that got a great bump in June 2024.

Coverage Details

- Annual Liability Insurance Limit: $2,000,000 aggregate

- Defense Expense: No Limit

- Cost of Bail Expenses: $250,000 of funds. A $2,500,000 bond usually costs $250,000 or 10% of the total.

- Incidental Expenses: $20,000

- Red Flag Coverage: Up to $15,000 in attorney fees and expenses

- Actual Loss of Earnings: Up to $750 per day, plus up to $10,000 to cover lost earnings if an incident prevents you from working for up to 30 days — whether due to injury or authorities restricting access to your workplace

If you want to learn more about the insurance part yourself see the full details here.

Will USCCA Drop Me If I’m Convicted of a Crime?

Plea Deal Coverage

If you take a plea deal that does not include a “crime of violence,” your coverage doesn’t end.

A crime of violence is one that “it involves the use, attempted use, or threatened use of physical force against another person.” Some examples include murder, aggravated assault, kidnapping, arson, robbery, extortion, unlawful possession of a firearm.

This is great since before any plea deal would end in coverage.

Impartial Coverage Determination

Before, what was or wasn’t self-defense was determined solely by the insurance company.

Now, as long as a USCCA Member and their attorney are permitted to argue self-defense as a justification and defense of the Member’s actions, and no other exclusions in the policy apply, the USCCA Member will be covered for their self-defense incident.

Coverage is also available until the final non-appealable finding of guilt.

Recovery & Recoupment

Why is there still a scary recovery & recoupment clause in the policy?

- This would be triggered by government or regulatory body forcing an attempt at recovery.

- Some states require this language.

- The insurance policy needs something to protect against fraud.

As of the latest update, USCCA has stated that the insurance company has never recouped any amount paid on behalf of USCCA members.

Next up I’m going to dive deep into are what other things you get with USCCA…and what membership tier to get for your end goal.

Removal of Previous Exclusions

Coverage is no longer affected if your self-defense incident occurs in a post office or federal building.

Also, firefighters and paramedics are no longer excluded while on duty. However, LEO and security are still excluded while on duty.

Free Pew Pew Tactical Handgun Course

BUT THAT’S NOT ALL! Sorry had to do that…

If you sign up for any USCCA membership you’ll also get free access to my Beginner’s Handgun Course which is normally $67.

I’ll take you from total gun newbie to someone safe and competent with handgun fundamentals.

Here’s a clip of how to fix a “double-feed” malfunction.

Every 2 weeks or so, an automated system will send you a coupon to sign up for my course for free.

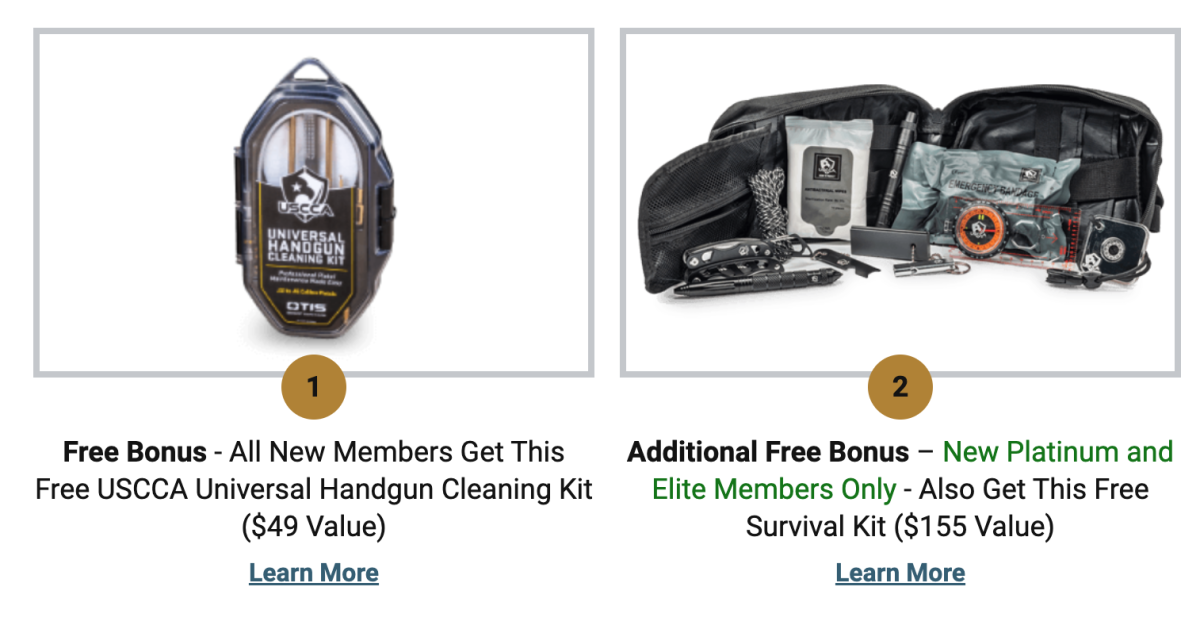

More USCCA Bonuses

Ok, there’s even more stuff now when you sign up. These offers change every month or so and I’ll do my best to keep on top of them.

Right now, all members signing up get a handgun cleaning kit and if you sign up for Platinum or Elite you also get a survival kit.

You can see the latest bonuses by scrolling down on the main signup page.

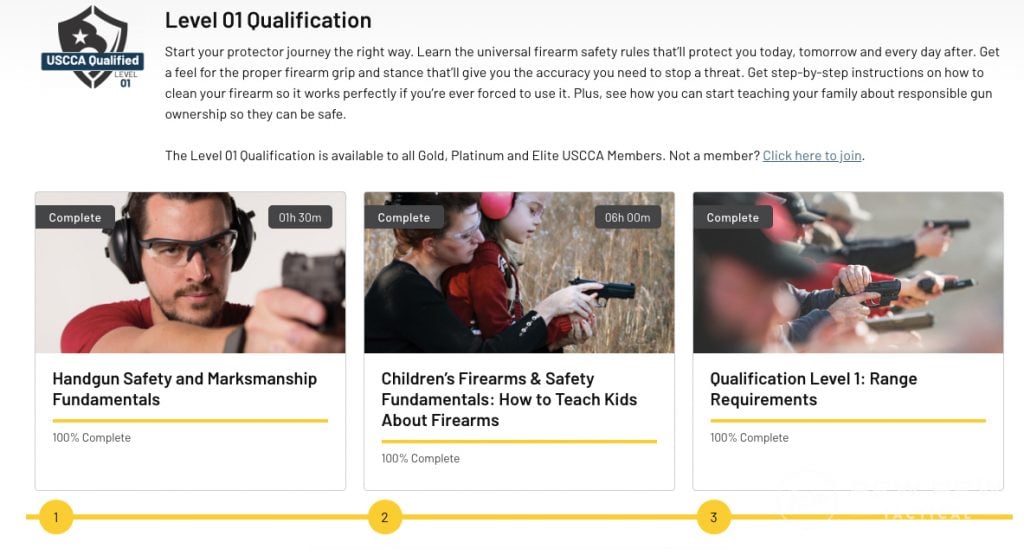

Gold Membership Perks

Now…back to USCCA! What do you get with the beginning Gold tier?

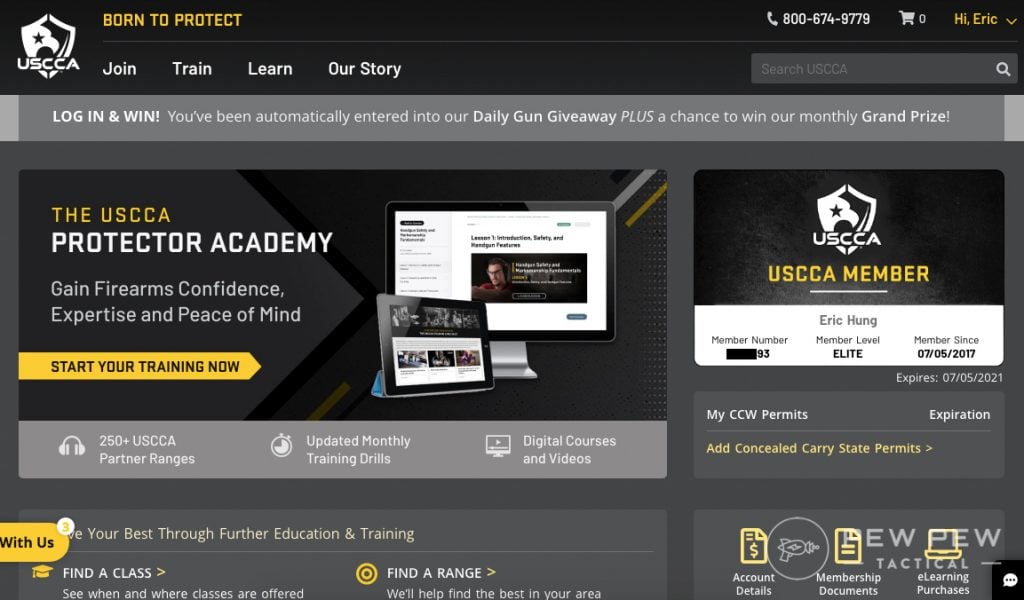

Once you log onto the USCCA site…it’s a little overwhelming with all the stuff.

Protector Academy

But that Protector Academy…that’s the good stuff.

With the starting Gold tier…you get access to Level 1.

The Handgun Safety and Marksmanship beginning video series is a great primer for everything handgun.

It’s a series of front-facing discussion, top-down views, and pictures of important concepts.

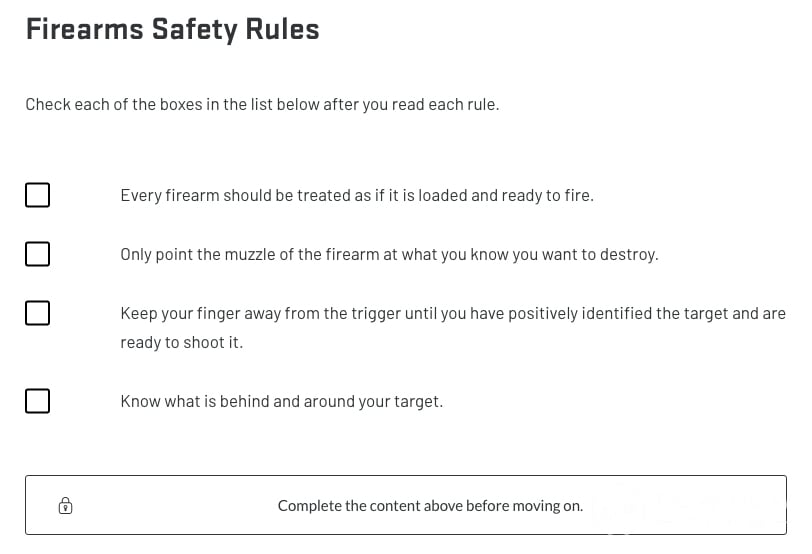

I also like how in the course they really hammer in the firearm safety rules.

If that’s the only thing you walk away with…you’re still good.

Plus you’re able to play at up to 2x rates if you’re like me and have gotten used to it on YouTube and podcasts.

Next up is the Children’s Firearm Safety & Fundamentals series which is great for parents of young ones like myself.

It’s definitely more engaging than the first one since the instructors are a real life couple.

They covered some good things for me:

- developmental stages vs age for when to start teaching children

- teaching mentality and different views when it’s children

- great examples of modified activities for dry-firing

Last up for Level 1 is the Range Requirements that you can fill in yourself.

And which consists of 2-hours instruction with a trainer, and 50 rounds into a target at varying distances with a 70% hit rate.

Easy peasy if you’ve got the fundamentals down. And you should…with both my course AND USCCA’s course!

Pass it and you’ll get a nice patch in the mail.

What else do you get in Gold?

Situational Awareness

Another great video series with Tim (founder of USCCA) and Kevin, editor of Concealed Carry magazine (and full-time LEO).

Here they covered really useful (and actionable) info like how to choose the best seat in a restaurant, mentality for going to “sketchy” places, and more.

Highly recommend giving it a watch since the best defense is to never get into bad situations in the first place!

When to Use Deadly Force

Another good series that puts gun owners in hypothetical AND real situations…then answers their questions.

I found it good to think over situations, see how my actions differed from others, and then go over some FAQs for general situations.

- What are your own rights?

- How should you train?

- What do you teach your family?

Other Stuff

Discounts and free shipping at their store. Pretty decent but nothing to write home about.

You also get their magazine digitally + paper copy.

Here’s the latest copy for me which goes in-depth into a case where a member actually used the insurance for a murder charge.

BUT…one thing I almost forgot was their 30 day money back guarantee.

Gold Verdict

You are probably after the most cost effective option at this point …but the courses are decent and you have a very nice 30-day guarantee.

Check out the full details here.

Now…what about the next membership tier up?

Platinum Membership Perks

Again, you get access to the Self-Defense Liability Insurance* like the gold plebes…but you unlock a bunch more educational stuff.

My favorite is the Proving Ground. But first…more courses!

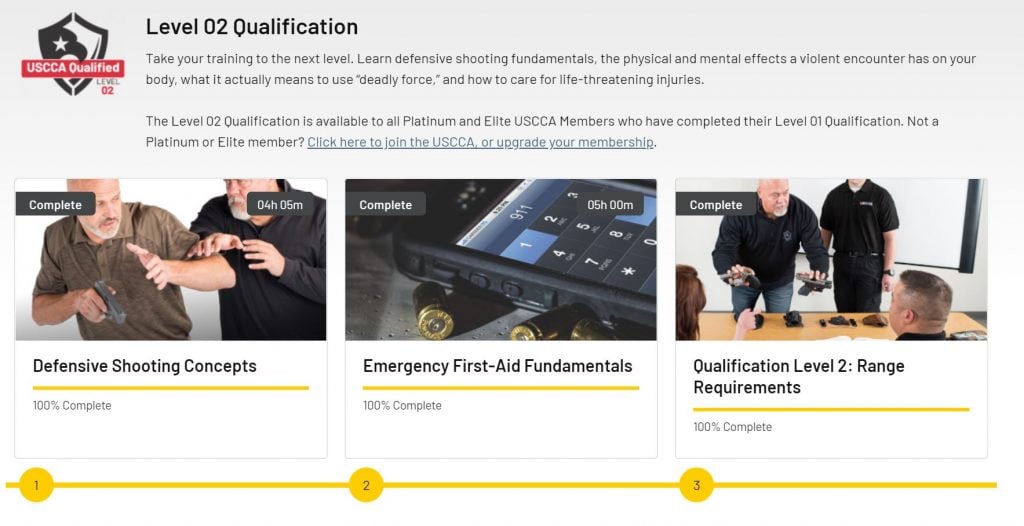

Level 2 Protector Academy

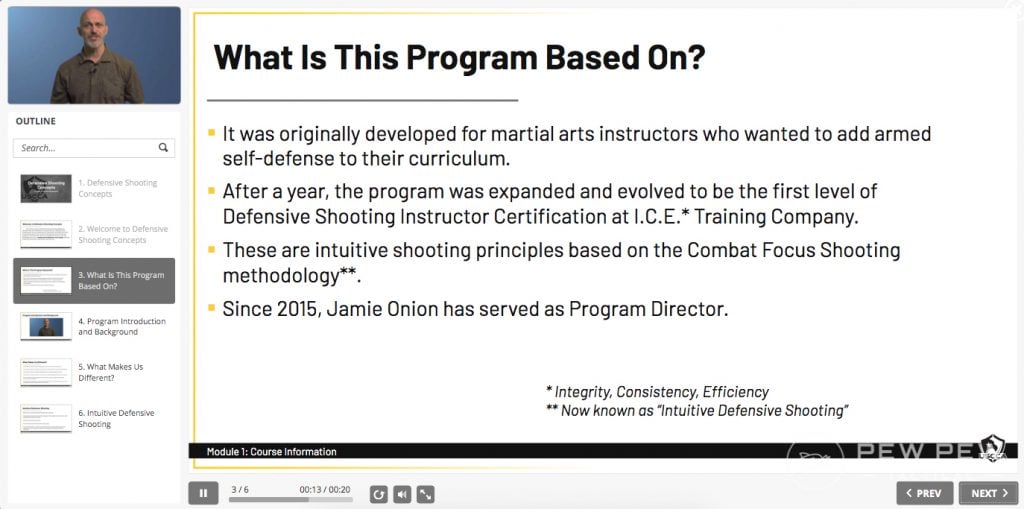

Boom! First up is a class with world-renown Rob Pincus that goes over defensive shooting concepts.

With a big emphasis on concepts.

It has a different player that’s a small video and Powerpoint slides.

It really felt that it was some content that was repurposed for the course.

Not saying it’s bad info…since it’s really good mindset stuff.

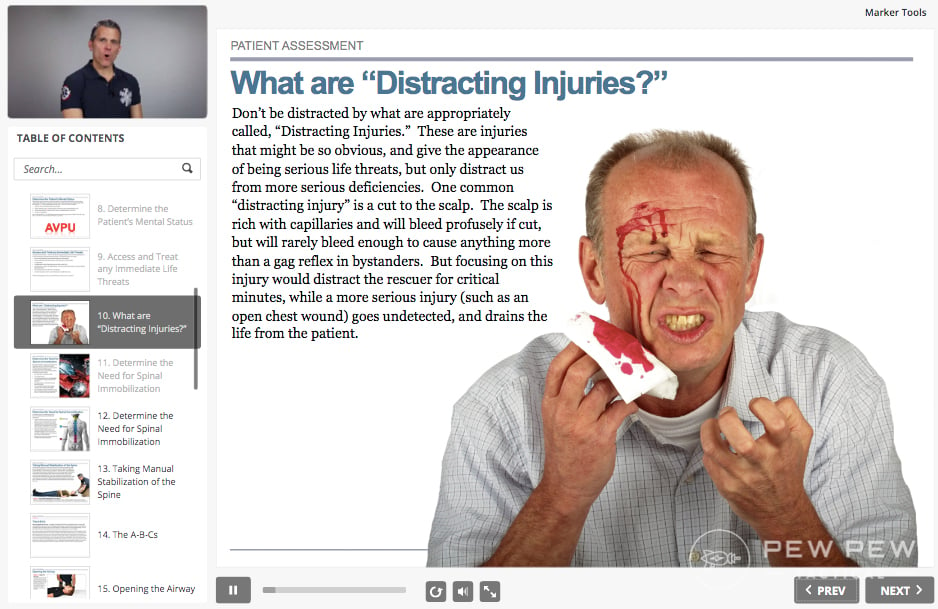

Next course is a medical one in the same player format that goes over some useful info if you’ve never taken a med class before.

Overall it’s good info on what you can do before real medical help arrives.

There’s stuff on assessment (scene safety, life threats, distracting injuries, etc).

And easy-to-remember acronyms like ABC (airway, breathing, circulation).

Then rounds it out with things like heart attacks, CPR, diabetes, and stroke. Before going into setting up your own med kits of different sizes.

Next up is the in-person range test which is more difficult now. However on par with concealed carry qualifications if your state requires those.

The Proving Ground

Ok…my favorite part of the Platinum tier.

It runs normal people through real-life scenarios. It’s entertaining and gets you thinking of “what would I do?“

Plus the break-downs at the end are super helpful.

There’s a bunch of them and you get access to them all.

Sometimes things get…hostage-y.

I won’t give you any more spoilers…but it’s good content and makes the Platinum level worth it for me if they keep producing Proving Grounds.

Platinum Verdict

You still get all the Self-Defense Liability Insurance* benny’s and some more advanced classes. But it’s the Proving Ground that makes it worth the jump.

Since you CAN downgrade/upgrade…it might be worth it to start with Platinum, watch all the Proving Grounds…and then downgrade.

If that’s your thing.

Otherwise Platinum is a good middle-ground for more info. Check out details here.

And remember…you get my course no matter which tier you choose.

Now onto the Elite tier!

Elite Membership Perks

The highest tier…you get all the previous goodies AND even more courses.

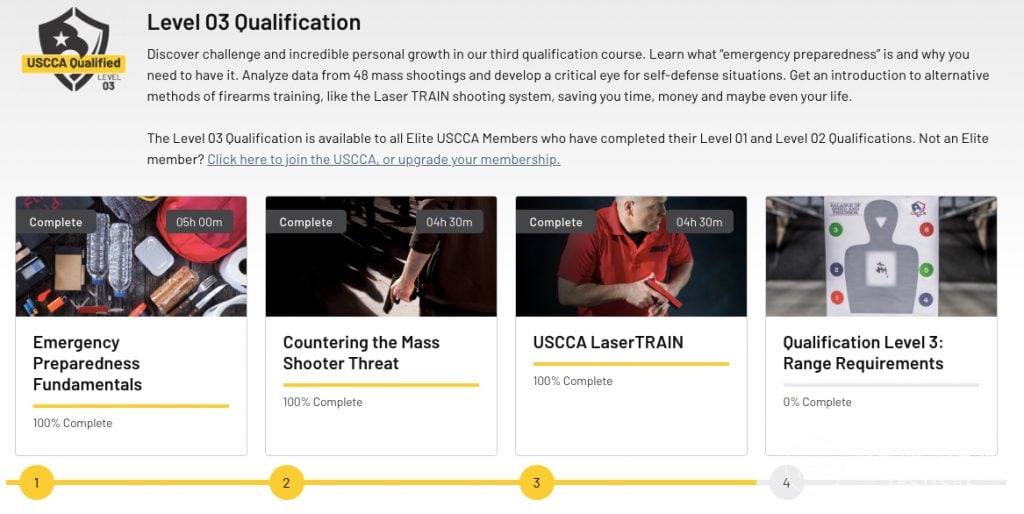

Level 3 Protector Academy

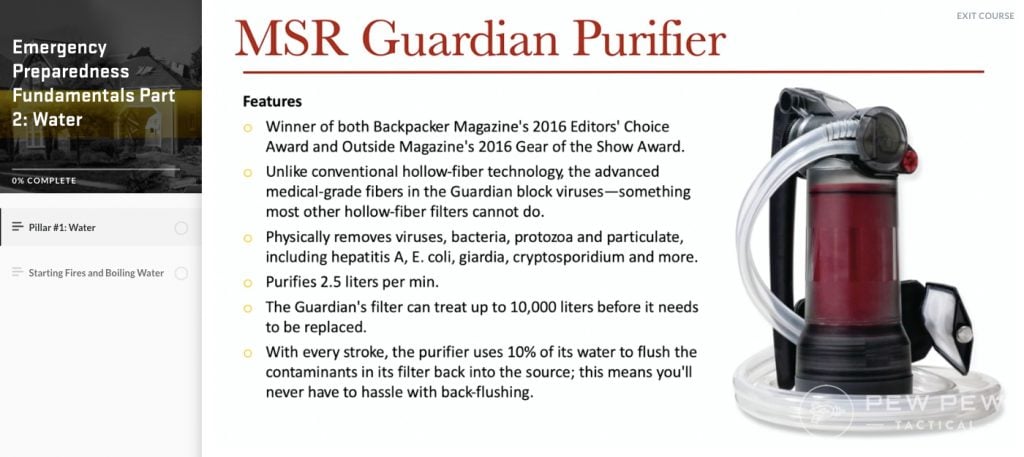

We go through our fair share of survival on the site so I dove into the Emergency Preparedness Fundamentals first.

They do a good job of going through the basics starting with water…and actually deep dive into what purifiers to get for your specific purpose.

Don’t forget about fire! I like how the instructor was outside using specific firestarters. Much better b-roll for this course.

And of course food!

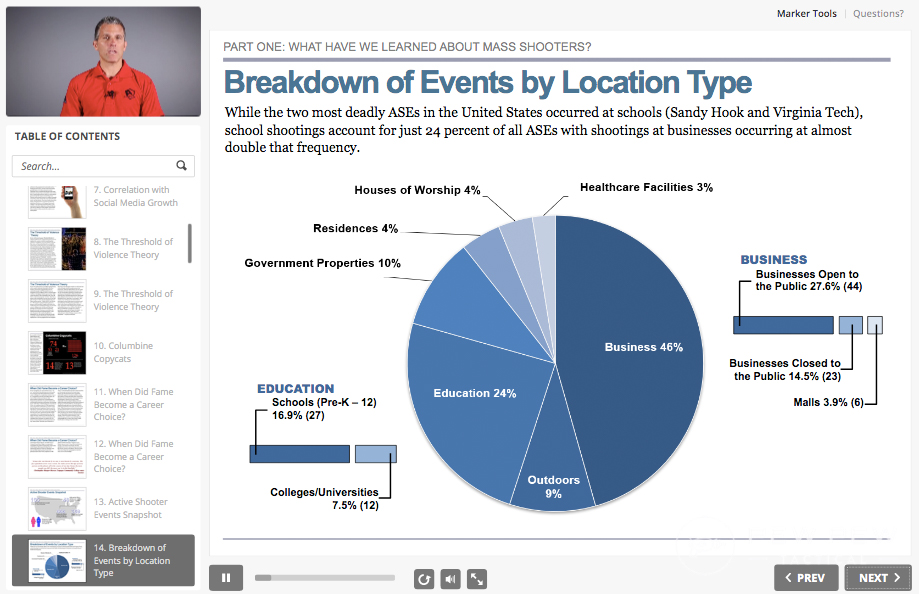

The next course is the Mass Shooter course…

There’s good stuff on why mass shootings are getting more prevalent but the above image was eye-opening info for me. With a much higher percentage of business shootings and a much lower percentage of houses of worship from what I thought.

Lastly, there’s the LaserTRAIN course which uses a SIRT laser pistol. I didn’t have high hopes for this one but it exceeded my expectations.

You can tell the instructor does this all day long and knows how to present information.

Now…how about the Level 3 range test?

I haven’t had a chance to do it yet but it definitely ups the ante with both speed and precision portions at 3/5/7 yards with a much more challenging target.

Mastering Handgun Confidence

Done with Protector Academy? There’s three more standalone courses you get with Elite.

These get more in-depth than before.

You have Kevin again learning about the fundamentals of handguns…but also the caveats that separate a beginner from the more advanced.

One tidbit even I picked up from the trigger pull section was to think of pulling the trigger from the front sight through the rear sight.

This equalizes your internal focus onto both your fingers and your eyes whereas if you only focus on the front sight you skew your focus.

There’s also more advanced drills done at the range such as the wall drill, bullet hole rill, walk-back drill, and reset drill.

Overall a good “intermediate” handgun course.

Armed American

Tim is back with the emergency prep guy for this series which starts off with securing your home.

Before diving more into setting up your own personal protection plan with the color codes of awareness and awareness of your surroundings. Things we’ve gone over before but now it’s more in-depth.

They also get into gun laws and the financial aftermath of what happens in a defensive gun shoot. Plus detailing what exactly are “castle doctrine” and “stand your ground” with a lawyer.

Next up is a little section on choosing your gun (which I felt was a rehash) and then a good section on the 10 concealed carry mistakes you can make.

#7…not trying our your defensive ammo in your gun. I know it’s expensive but you have to make sure it works…and that you know the difference in recoil!

Armed and Ready

Last up…this course seems to be from DVDs since they talk about disc numbers. On the surface it seems like another rehash but there were some good tidbits.

The “Hard Truths” lesson gets you a little riled up and in the protector mindset after utilizing some news footage of bad guys doing bad guy stuff.

Before getting into guns (again) and holsters (yay).

They dive into all the malfunctions with actual on-the-range footage.

As well as some advanced stuff like movement and cover. Finally.

Then they end it with some pre-threat indicators since the best thing is avoidance…as well as some home staging.

Last up is what exactly is “deadly force” and what happens after a defensive gun use (lawyers, cops, phone call, and family plan).

It’s good to think of it now before something bad happens!

Other Stuff

I just about covered it all!

And yes…you still also get the self-defense liability insurance that comes with any USCCA plan. See details here.

Elite Membership Verdict

Some just want it all and you get it with the Elite Membership.

The additional Level 3 Protector Academy courses are quite good…as well as the three additional standalone courses that get much more in-depth.

But my advice is the same as the Platinum…

Since you can upgrade or downgrade I would soak up the info…see if it’s worth the new stuff and then downgrade. You’ll still have your insurance regardless of what plan.

USCCA In Person Classes

Even if you don’t go for the membership, USCCA is taking the lead in coming up with comprehensive curriculum and training tons of instructors across the US.

Their main in-person course is the Concealed Carry and Home Defense Fundamentals which goes deep into handgun basics and whose goal is to help you make it home safe every night and remain safe at home.

I attended their newer AR-15 Fundamentals course and two of my fellow Pew Pew Tactical co-workers got instructor certified.

Yes…AR-15s are awesome for home defense!

It’s a great course for all levels and the instructor certification process was very rigorous over three full-days with plenty of prior homework and assessment.

Final Thoughts

It took a lot of words and video watching to get here…

But if you’re only looking for “concealed carry insurance”…know that you get personal insurance* solely by being a USCCA member even at Gold tier. Details here. Remember I’m not an insurance agent…

But for those who are looking for that AND education…it’s a question of how much you want to learn.

I would get the Platinum tier to start so I have access to Proving Ground and Level 2 Protector Academy.

But if you really like to learn everything you can’t go wrong with Elite.

You can upgrade/downgrade as you wish and there’s a 30 day money-back guarantee.

PLUS…you get access to my Beginner Handgun Course ($67 value) with any tier. I get emails of signups from USCCA and then auto-send coupon codes every 2-3 weeks so please have patience!

The Fine Print

*The USCCA is not an insurance company. A policy has been issued to the USCCA. That policy provides the association and its members with self-defense liability insurance, subject to its terms, conditions, limitations, and exclusions. I also have a working relationship with Delta Defense & the USCCA. CA #4272012.

LATEST UPDATES

- February 2025: Updated with changes to the program that included policy updates and pricing changes.

- June 2024: Updated with changes to the program that included policy updates and upgraded coverage amounts.

{kind=link}

252 Leave a Reply

I've used you guys as a shooting resource for years. I have referred plenty of people to you in order to "level up" their shooting knowledge. And you were part of the reason I originally went with USCCA.

All of that being said, I would really like for you guys to do an objective piece on Kayla Giles and Alan Coley (maybe even contrast it to what Attorneys on Retainer had to say).

USCCA started off strong for alot of us. But some of their actions (not just policies) forced many of us to look elsewhere for peace of mind in a worst case scenario.

Yes, that is true with USLawshield at a ccw class. I signed up for their insurance and the only thing I received was a paper card included in the sales flier. No insurance policy .

This is precisely why CCW Safe is self funded - no anti 2A groups can pressure the insurance company to deny coverage. The NRA offered some sort of coverage, but the coverage disappeared when anti 2A groups pressured the insurance company to drop the NRA.

I am concerned that USCCA would bail on me, like they bailed on Kayla Guiles.

Sad to see so many reputable vendors pushing USCCA. While their training content is great, the coverage is still governed by an insurance company who must follow all laws and regulations that apply to insurance. For anyone shopping for legal coverage, I would recommend skipping past the endorsement and even past the marketing materials on USCCA's website. Look at the contract and coverage from the insurance company. There are still a lot of gray areas that could (or arguably would) result in loss of coverage after an incident. Read the fine print. Better yet, find an attorney to help you interpret the fine print.

If I loose in court is the uscca going to try to recover the cost by sewing me?

This article about the different levels of USCCA were really good. In-depth. Kept me reading! I am a member at the gold, just might upgrade. Thanks for all the info. Very interesting!

I respect Pew Pew and read regularly. However this is the first charged and overly long endorsement. I just got my CCW yesterday. I humbly suggest that if you carry, do very serious in-depth insurance research on your own. Because you are definitely getting charged with multiple felonies starting with the presentation of your weapon. Be safe.

All I can say is I was with USCCA for years and then all of a sudden they raised my rates exponentially. I called them and said I’ve never had to use you and been with you for years. Why are you raising my rates?

and they could not give me a straight answer they just said that everything went up. WTF?

Needless to say I canceled them on the spot. I wasn’t very happy.

I guess if you live in a high crime rate area, you would need some sort of insurance, but in my book, I’m saving a lot of money by not having it.

Hi Eric, So I live in New Jersey. Does your statement at the beginning make my interest in your insurance through you unattainable? Thank You, Steve

I researched quit a few CCW insurance carriers and found USCCA to be the best value for the money. Their platinum service comes with a ton of video training materials and more importantly they have 24/7 attorneys near me in case the worst happens.

Schilling for a horrible company like USCCA?

I already unsubbed from your YT channel, gonna unsubb from your emails now too. ✌

Lots of negative opinions with generic statements of denied coverage etc. I’ve yet to find an actual, documented case of this. If they exist I’d like the replies to include the actual case, court or anything to support their statements.

Kayla Guiles, there are others i could look up, I could also look up the case number to Kayla's case, but you're sounding lazy and entitled.

Kayla is a tiny woman who was being g beaten in front of her kids by her ex who was a 200 pound pro mma fighter uscca denied her claim and refused her representation, there are many other similar cases.

But go ahead and stick your head in the sand and ignore facts.

She was CONVICTED of premeditated murder! That anti USCCA myth was debunked in 2022! She purchased the USCCA policy beforehand while planning the murder. No insurance company covers you if you’re engaged in a crime, have a competent adult explain how insurance works to you. Save the name calling for your Facebook page.

Anything to justify your wasting money on garbage huh?

You sound super emotional about this, you should probably lay off the soy, and eat a steak.

Just because someone is convicted of something doesn't mean they're guilty.

You probably think Trump is an "actual" felon?

Kayla was convicted because USCCA threw her under the bus.

Watch the "Attorneys on Retainer" youtube analysis on the case that's 2 actual attorneys (Marc J. Victor and Andy Marcantel)

The Lawyer they originally assigned to Kayla said they had a great self defense case, they then removed him from the case.

Until that case is overturned on appeal (not likely given the facts) your argument has zero merit….. and seriously, resorting to name calling diminishes your argument and character even further.

You have to pay up front then they pay you back if they decide too. There's better places out there and they pay for it. You don't pay anything

"You have to pay up front then they pay you back if they decide too."

That's not true.

I've used them...there was nothing to pay "up front" - they started paying for stuff immediately (as soon as I notified them).

There have been people that did 'pay up front' before they notified USCCA, and they were paid back. USCCA, nor any 'self-defense' plan an 'insurance' or not, can't do anything unless you notify them.

I called their 24 hour emergency number, told them what happened, and asked they provide a lawyer as I did not have one available (they will pay for any lawyer you select, it does not need to be one that is associated with USCCA), they provided one from their network of lawyers associated with USCCA. I was never asked to pay anything, even the lawyer told me that, nor did I pay anything through the whole ordeal. USCCA insurance picked up the tab for everything from beginning to end, even paid for a new gun (as the one I used was in police evidence lockup and had not been returned after it was all over - eventually it was returned, but I did get to keep the one USCCA insurance paid for.)

Eric, I normally like you stuff, but not this piece. The stuff that has come out as of late about how the insurance underwriter for USCCA is denying claims at such an alarming rate, and the result is convictions and incarceration for USCCA members that believed in that product. And who had genuine legal self-defense claims, yet were abandoned by USCCA. The insurance underwriter has pulled some pretty shady dealings! I have tried talking to USCCA about all this and have been very rudely ignored. YouTube gun folks and many 2A lawyers are reporting more of the same. USCCA seems to be pretending that it isn't happening. Any time I see fluff pieces for them I start to seriously question the integrity of the writer and organization they represent. USCCA lost their integrity some time ago and are seriously bad for the 2A community. Eric, I hope you haven't lost your integrity.

I currently have CCW Safe but was recently looking into coverage if in a "sensitive" place. I live in CA and I can't legally carry in what the state deems are sensitive places. Plus, they recently passed SB2, which is going to exponentially increase those sensitive locations. CCW Safe clearly states it only covers you if you're in a place that you're legally allowed to carry.

After reading USCCA's terms, it states exclusions to include "unlawful possession of a firearm in violation of 18 U.S.C § 922 or other applicable federal law." State law isn't specified so will coverage remain if I'm in what the state of CA determines is off-limits, but not federally prohibited?

If SB2 isn't stayed, just being in any public place that doesn't have a sign posting stating you can carry will mean you're illegally carrying a firearm in a sensitive place. :(

I would go attorneys on retainer it is not a insurance company there a lawyer that helps u and want drop do not get this crap here

All about selling more crap.

Do you ever get tired?

One of the things that ran me away from USCCA was the avalanche of ads that continually appeared on my screen. I went with CCW Safe, after doing my research. And I'm glad I did - their coverage has improved.

Yeah i cancelled USCCA and here's why. Gotta read the fine print boys and girls.

#1 if a DA charges you with a gun crime and it's a criminal charge not a civil one (pretty much all gun crimes for the most part are criminal) USCCA WILL NOT COVER you under their insurance PERIOD, no if's ands or buts, even if your innocent. NOPE. You don't think the local crazy DA's don't know the insurance policies of USCCA. They can charge you criminally for anything. Doesn't mean it will stick but it just means you get bankrupted because you can't use USCCA insurance because of a "clause" they slipped into their insurance paper work recently.

#2 if you are found guilty of a non-criminal act (the only thing their lousy insurance covers) YOU are REQUIRED to pay USCCA back in FULL, 100% for all legal expenses incurred. So again what's the point of this garbage insurance? I concur with what Joe said below. He is correct.

#3 If you utilize USCCA insurance to pay for your attorney's fee. USCCA dictates how you interact with the attorney, how much time you are allowed to spend with them, what conversations are allowed to happen, etc. Clearly violates client attorney confidentiality, but USCCA doesn't care.

Like I said. Just like the NRA, the USCCA takes your money and doesn't really care. Sure they print a few magazines, make a few training videos, hold conferences, do some lobbying, but whoop de doo. The insurance is a total scam if you ask me.

Good to know!

If USCCA is out, who do you have your coverage with?

To hell with the USCCA. They backstabbed their members a year or two ago when they surreptitiously and without warning changed their policy to include a reimbursement clause should the insured be found guilty or forced to plead to a lesser charge. I cancelled my USCCA insurance when I confronted them with that info and they refused to give me any straight answers.

Wow! Thanks for saving me! I almost subscribed to USCCA before reading this. Total rip off. I would never knowingly agree to a reimbursement clause like this. Just… wow! Oh, BTW, who would you recommend?

It would appear that you are at the mercy of the lawyers and you will be bankrupted regardless of what insurance you have. I cancelled my USCCA insurance as well. What's the point of paying it when it covers virtually nothing and if your found guilty of a civil crime (they don't cover criminal charged crimes even if it doesn't stick), you have to pay it back in full to USCCA. Pointless.

CANCELLED MINE TODAY. Goodbye USCCA. You pulled a fast one on your members see ya!

I love this site and it's been my trusted go-to for advice on all kinds of gun-related subjects. I purchased the Handgun Course and it was well worth the money, very grateful for that. I trusted this site so much that I'm really disappointed with this review of USCCA as an insurance carrier. It's shamelessly sales-y and concentrates on perks rather than what matters most if the main point of the conversation is about getting the best CCW insurance coverage. I noticed that the comparison article covers CONS for other carriers but not USCCA, whose coverage has one major, deal-breaking CON for me: they reserve the right to go after the insured to recover defense expenses if the insured is found guilty in a court of law. That's a huge consideration that those looking for insurance must be made aware of, and one does not need to be a licensed insurance broker to share this important detail.

I, too, was initially swayed by all the bells and whistles of USCCA membership (namely, all the educational content covered in this article), so it pained me deeply to discover this game-changing clause in their policy, which even much cheaper insurance companies don't have.

Wish USCCA offered an education-only plan but, in the absence of that, all the educational content in the world means nothing if one should ever be in a situation where a jury needs to decide our fate over an action that took seconds to contemplate and carry out. Should that ever happen, last thing I want hanging over my head is the possibility of being sued by my insurance company at their discretion to recover costs. I'll take the world-class, no strings attached defense provided by CCW Safe any day, even if their perk roster pales in comparison to USCCA's; I can get my education elsewhere.

That said, I understand this is a very personal choice and the great majority of us will never find ourselves in a real-life draw situation requiring defense. Judging by USCCA membership numbers, the vast majority of people feel the perks are worth the gamble, and to each his own. However, guiding others who trust our judgment in such an important matter as which CCW insurance to get is a huge responsibility (at least to me), so omitting the one detail in the discourse that could make all the difference is a significant fail in my book.

I read your review on CCW SAFE and you said that it was your preferrred insurance plan. Here is your quote: "Of course, just because CCW Safe is my preferred CCW insurance plan, doesn’t mean it’s the right one for you." Now you are saying that you have an Elite uscca membership and it is the best one. Which is it? Please clarify

Different author; ERIC HUNG, here, PAUL YEN, CCW safe.

He is paid for both. So he won't bash or downplay either.

Both are substandard.

I read a lot. I remember some and then put it together and expect, no demand it makes sense. For all you need to decide when you chose to pull a gun are you prepared to take a human life. Gun out pointed at a criminal is not the time to make that decision. Far as insurance I recall reading an article by an attorney. In a self defense shooting, it is a safe assumption that the prosecutor will go after you with an unlimited budget especially to avoid public outcry. Far as insurance, I would like to hear from someone who needed and used their services. I've read unless you hand them a perfect case, they will not defend you.

Your posts are always well done. I tend to read a lot, remember some and expect not demand that it fits together when I made a decision. Today's reality as I understand it. If, you ever need to pull your gun, first of all that is not the time to decide if you are prepared to kill someone. Assuming you did everything correctly, you will be prosecuted and they will do anything possible to destroy you. The prosecutor's budget is UNLIMITED. Far as insurance, an article by an attorney says, if there is any question at all, they will not defend you. A criminal-you are at a distinct disadvantage. Did you follow the advice on page 47 of the manual? You know the third paragraph. The criminal is a criminal-he maybe on drugs, etc and he being a criminal DOES NOT CARE.

What do you do if you’re a resident of New York?

Of all the areas in the country, Communist NY is one of the states that you would need this type of insurance the most.

Any suggestions would be greatly appreciated

Their insurance is a scam. Read my post above. #1 and #2 points.

Move! Duh

I've been a USCCA member for a number of years enjoying the knowledge of the Delta Defense Team standing ready to assist you should the worst situation happen - you shoot someone. I appreciate the attitude of restraint and advice on avoidance of situations that would put you in a position to find it necessary to use deadly force. The articles on their website and in Concealed Carry magazine are constant and excellent reminders of the huge responsibility everyone who carries a firearm must shoulder. USCCA also discusses every day situations and the legal options and ramifications of concealed carry. One recent article that should be a must read for everyone was about the 6 things that will happen to you when you shoot someone. I highly recommend to anyone that carries a firearm to belong to USCCA if it's offered in your State (not available in every State - surprisingly). Regardless of who you think you are, if you shoot someone, you are going to need help. USCCA will prepare and assist you in that regard.

USCCA is simply a weapon training and informational website. Not a bad one at that. However, they are an agent for Delta Defence. If you need help after an unfortunate situation of defending yourself, it would be Delta Defence you would deal with . Not USCCA.

What is the year and month of article "6 things that will happen to you when you shoot someone"? It is always good to site your sources.

No they won't. They specifically state they will not cover criminal cases. Which ALL self defense cases are.

You are lying, or ignorant.

All you really need is an umbrella insurance policy from your insurance agent. Almost everyone has car, home, or rental insurance. All them up and compare rates. The rest of the "training" they offer really isn't all that good.

A few issues with USCCA:

1. This year they jumped rates dramatically (and abusively).

2. They spam the crap out of you. Prepare to adjust their filters.

3. They waste a lot of effort on cheesey products and promotions like a cheap ripoff site.

On the plus: they have discusses with a self-defense lawyer that are good. Coverage for the wife is reasonably priced.

What about a major clause. In the insurance package; where if you PLEAD GUILTY OR FOUND GUILTY, you can be forced to repay everything back to the USCCA!!

Scary there is no disclaimer in here on whether the author is getting compensated in anyway by USCCA.

I just bought the Elite package from USCCA. Ya 500.00. I feel better. I like the fact I can cancell, ifI really need $.

USCCA and CW Safe both seem to have good plans. What draws me to CW Safe is the unlimited defense expense. USCCA has a $250,000 payout limit. Is this amount realistically good with the current mainstream & social media? We've seen all too many self-defense scenarios on video which turn into high profile cases. Another issue with USCCA is if I'm convicted or plea bargain, they won't pay my defense? I'll need to re-read CW Safe to see if they have the same clause.

I have been going back and forth between these two services. I am leaning heavily towards CCW Safe as I cannot find anywhere that restricts a plea deal or guilty verdict. As a matter of fact they even state they will cover an appeal.

Good comments most likely leave uscca and go ccw safe because you dont have to pay back costs if convicted of a lesser charge.

If you plead to a lesser charge, say a misdemeanor, because going to trial may be very risky, even though you're in the right, because you took a plea deal, you are not covered, at all, and owe all expenses paid back to the insurance company. You can find that hidden gem on Page 11, Section I (as in "eye') Sub Section 1. In other words, if you don't go through to trial and prevail, none of your costs are covered. None. You have to repay everything.

This is troubling. I just joined, and now that I see that language in the agreement, I may cancel.

If a company promises to provide legal defense for a policyholder after a firearm incident and a court later determines the act is criminal, the company may have sold an insurance product that is not in the public interest and that doesn’t comply with state law.

If a company promises to provide legal defense for a policyholder after a firearm incident and a court later determines the act is criminal, the company may have sold an insurance product that is not in the public interest and that doesn’t comply with state law.

What options are available for insurance protection in NY, NJ, and WA?

What do you recommend for residents in these states to protect themselves against the legal and civil liability expenses?

Hello Ken,

As someone who recently moved out of the "People's Republic of New Jersey," I can only speak of that state. So, it's basically a non-issue there because unless you are law enforcement, retired law enforcement, or work as an armed security guard, you cannot get a CCW. It's impossible. You can carry concealed in your place of business and on your own property, but even still, NJ is not a "stand your ground" state and there is no "castle doctrine" there. The best you can do is (along with the NRA) to join the NJARPC. They have lawyers on retainer for questions only. Other than that, you're basically screwed if you exercise your SA right to self-protect., unless Evan Nappan takes your case pro-bono. I was able to get Texas Law Shield there, but I got out of NJ and moved to South Carolina. Now there is a great gun state, got my CCP with no problem. I gotta figure NY and CA are similarly horrid to NJ..

In your criticism of TLS you linked to a story on “TheTrace”. That source is a Bloomberg anti-gun rag. Calls into question the rest of your article.

The Trace does have an anti-gun slant, but their facts, in this case, are not incorrect. TLS was the subject of a class action filed by Texas CHL holders. I don't know the details or the outcome of that lawsuit. Here is a second source for all of the information: https://www.law.com/texaslawyer/almID/1202733632179/Judge-Grants-Class-Certification-in-Texas-Law-Shield-Suit/?slreturn=20150713103623/

All I want to do is buy some insurance and it is not easy to do

Look at Giles v. USCCA and you might change your mind. They refuse to pay.

Missing many facts here. It appears she may have purchased the firearm and membership, then baited her husband into a confrontation, counting on USCCA to pay her legal fees. USCCA may be privy to some information from the prosecution in the case that contraindicates her legal status to their services. The full details of this story are yet unknown to the general public.

4 years later and that's not the case at all.

I have been shooting for over sixty-five (65) years. I am very much experienced with firearms & I spent over forty (40) years in the insurance industry having founded and run my own insurance agency. I highly recommend a membership in the USCCA and obtain their insurance. I am an elite member myself. Good Luck & Stay Safe.

I hold an Elite membership with the USCCA and I wouldn't think of anywhere else. Tim Schmidt founded the USCCA and continues as the head of it. I was swayed toward the USCCA when I was shopping because of him. The coverages were close but he was a hard worker, smart, started the USCCA with basically nothing but an idea and made it what it is. The others didn't have what seemed like as well thought out a business plan. Tim has slowly and methodically worked toward his goal and reached it. He sacrificed some family time but not so much that he didn't benefit from having one. I'm a retired/disabled businessman having had virtually the same experiences. I can't envision Tim offering his membership anything but the best he can. One of my own companies was a family founded and owned (by me) insurance agency. I was in that business for over forty (40) years. I have also been around firearms for even longer. I'm now in my seventh decade of life. When I was four(4) years old my fathers uncle took me to some land he owned, and I shot a firearm for the first time. Firearms have now been a part of my life for over sixty five (65) years. I was taught to and I practice safety at all times around firearms. However, just in case a situation arises that I can't avoid, I'm glad I have the peace of mind of having a membership with the USCCA.Stay safe.

You really have to be lawyer with insurance expertise to determine if any of these are of any value.

Everytime I get ready to buy a policy I read one of these reviews and come to the conclusion that you will just be lucky if it pays off.

I have a significant practice as an expert witness regarding insurance coverage disputes. I would like to see a copy of the actual policy. The problem here is that if someone is accused of a crime, it may not be legal for anyone to provide insurance against an illegal act. If the situation involves an allegation, other than simply having committed a crime, then the insurance may provide coverage under a reservation of rights. It might be better to sell this as a pre-paid legal product, which would not necessarily run into the same legal ramifications. The NRA problem ran into serious problems because it was allegedly providing insurance for criminal activities, which is considered against public policy. This is a very complicated subject and I fear few of the people commenting are actually qualified to have an opinion.

Have you asked the company for a copy of the actual policy? IF so, what did they say?

USCCA IS HORRIBLE. I emailed them 3x asking them to answer a few Qs before I make my decision to join, and NO ONE EVER GOT BACK TO ME. I even “chatted” with a rep who confirmed the email address was correct. Both CCWSAFE and US LAWSHEILD had comprehensive replies to my questions within 36 hours. Lesson learned: USCCA will take the time to bombard you with marketing emails but cannot spare a few minutes to answer questions for a prospective member.

(Note: Due to disability, I am not able to call; this was not an issue for CCWSafe or US LAWSHEILD —- they were there for me when I needed them.)

Update: USCCA DID get back to me, it just took a bit longer.

NOTE: One of the BIGGEST DIFFERENCES between plans is DO THEY COVER COSTS & EXPENSES (C&E)? This is a HUGE amount of money that most people could not afford. — so DO read the Terms & Conditions before signing. Plans either Exclude C&E completely (meaning you pay all C&E out-of-pocket as you go along), or they may Include C&E in with attorney fees UP TO your max limit (which means you have less money for attorney fees), or they may Cover C&E apart from attorney fees which is the best of both worlds. Which you choose could make a HUGE difference in your immediate out-of-pocket expenses.

You need to add some precision to your email. I cannot figure out if you were comparing CCWSAFE and Lawshield to USCCA or the different plans within USCCA.

Thanks for this post. Now I'm reading the insurance policy that you link to because in my day job, I teach insurance. I'm very interested to dig into the details of the policy. Right off the bat, there are a couple of items that concern me, but I'll hold off judgment until I read it all.

It is interesting that I would not be getting my own insurance policy, but would become an insured on their policy. That has its ups and downs, but more later as I dig.

Hi Eric,

would you know if a "significant other" would be covered? We're together, but she isn't my wife as of now. Also, I became a resident of Florida, but she is still a New Yorker. If we were both up in NY visiting family, would we be covered at home in NY?

Thanks for the article.

Much of the information on this site is misleading. USCCA has been sued multiple times for failure to provide coverage. The incidents you mention with other similar groups, example TLS, that case was dropped and TLS was absolved of any wrong doing. USCCA also allows ANY attorney to be a part of their program. Meaning you may or may not get the best defense possible. I know a guy that used to be a USCCA member that left because when he called for an incident was told by a lawyer that the member would have to PAY the lawyer to be represented aside from the membership he pays.

Why not take a good look at the Armed Citizens Legal Defense Network. They are the best! I'm a member for over 8 years and will continue to be a member for years to come. Check it out.

The Feb 24 2019 article states you went with CCW Safe...this article says you've been with USCCA for quite some time? Do you carry both?

Two different people writing the articles

Coverage for my wife, being in home. Does that mean if she is in the garage or out in the yard and needs to defend herself she wouldn't be covered?

I read up on the US/TX Law Shield class action suit in 2013. Apparently they never learned their lesson because at the CHL class that my partner and I took in 2016 they were there and painting a very scary picture. They told us all that basically if we didn’t take advantage of signing up that day that we would be on our own and not offered their “deal” ever again.

I have USCCA the million dollar plan.. Here is the problem.. What happens when the DA offers that famous Deal.. Plead Guilty or risk Life in Prison.. Will the Atty try to pressure you to plead to something you are not guilty of to avoid the risk. I think the answer there is clearly yes..

More importantly however can USAA opt to refuse further legal financial support if one refuses to "Take the Deal" ?

Don't know the answer..

I would like to know if you have any alternatives for the state of New York if there's any.

Idk...move away?

so basicly what im getting out of this is if i have use my weapon in self defense i better be sur ei save a bullet for myself! it appears that even if im attacked and defend myself im basiclly screwed. I have held my Sacramento county California CCW for over 20 years and luckily have only had to draw my weapon twice both times showing the attackers i was armed put an end to the situation. In both cases i did not draw my weapon until they had pointed their weapons at me i never fired a shot.

I was just informed by USCCA that my membership could NOT be renewed any more because I am a NY State Resident. Apparently, they are now no longer able to issue protection and coverage for NY State Residents due to an "issue" (they would not be specific about it with me) that they had with the "political system" of NY State. So for any one who lives in NYS, you no longer have ANY coverage !!! Does anyone out there know what the "issue" was that the USCCA had with NY State ?? Any replies would be appreciated !

I signed up with them when you guys first reviewed them a while back and have not regretted it. Good company and great for the different levels of coverage to meet the needs/price point of different people.

These guys have too many restrictions. It is easy to go over their coverage limits with a trial. Think of the Zimmerman acquittal at $1.7 million. And if he had had a mistrial and the prosecutor decided to go after him a second or third time, he'd have run out of coverage with these guys. That's why I picked CCW Safe who have no limits on defending you in criminal and civil courts.

These guys are in the middle of a lawsuit where they decided not to cover one of their clients.

Way to pushy for me. Free guns every day? Who is paying for them? Their customers.

Great article. I signed up immediately and am very happy I did. Thanks.

I just joined uscca but unfortunately did not see this site first. I went with the elite annual plan

For 150$ more per year it basically doubled the coverage

I decided to go to the max since I reside in CA and own 2 small businesses. To much to lose not to spend the extra 150$. My hope is I will never have to use/test it. But like any insurance you only need it when you need it

Just signed up for the USCCA through the link - hope the noob offer is still valid

too pricey and limited coverage, Texas/US Law Shield better in my opinion

I joined using the link... hope the noob offer is still valid. How does that work?

Great update to the original. I actually picked up USCCA when you published the original article and have never felt bad about my decision. I have however, wondered if you still used them or still felt the same way about their covereage, so a great update to this article. I am still with USCCA and am actually about to add the wife who just recently picked up her CCW. As always, thanks for the great research and comparative work that you guys do for the rest of us!

I rock with USCCA as well. I maxed out with the Platinum tier. Love the helpful tips and seemingly endless educational resources. I feel a certain peace of mind knowing they can help me navigate through the legal minefield should a SD situation occur

My mistake, I meant the ELITE tier

Eric: Good article. I was surprised that you rarely carry a firearm so you must live in Kalifornia! I would suggest that you move to a constitutional carry state, or at least a state where it is easy and inexpensive to get a concealed handgun license. Never leave home or be in your home without immediate access to your firearm, as your life and the lives of your loved ones are at risk! Train like you will have to use your pistol and long gun, and hope that they will never be needed!!!

can you get gun insurance for just at home protection as i don't carry but have at home

USCCA covers in the home as well as when you CC!

I have the same question plus. Can I get home protection in California and am I protected if I am carrying my gun to the range legally in the trunk of my car and take it out to defend myself or my family?

Sad that one needs "self defense" insurance. What's next? Criminal insurance?

So, went to sign up with USCCA, but got as far as putting in my address. Turns out they can’t start new policies if you live in New York.

I've been a Gold member of USCCA since May 2019. What happens if it is determined that you acted in self-defense and it takes a long time to get your firearm back or never do from the police? Anyone knows?

I am retired LEO but have been out of it 20+ years. Used to be that police did not return confiscated weapons until ordered to / released from evidence by the a judge. I know that you can incur resistance in that regard from police departments but that usually stems from past experience with you and means that they may be petitioning the judge for a different action, It is a judge that will restrict or delay the return of your firearm in such cases that you were not convicted of whatever the offence was that the firearm was taken.

USCCA will reimburse you up to the Manufacturer's Suggested Retail Price of your gun if it appears it will not be returned.

Eric,

I "think" you got most of it right but I am a little confused about your comments RE: Bail Bonds.

In the article you explain that ...

$25,000 / $250,000 Bail Bonding

The asterisk says “Reflects 10% of the face amount of the bond. For example, $25,000 reflects a $250,000 bond.“

It’s my understanding you’ll only get 10% of the bond (whatever it is), and only up to $25,000 which would mean a $250,000+ bond.

What does the + mean? If the maximum coverage is 10% for a $250,000 Bond you're capped @ $25,000. If I got this wrong please forgive me, otherwise, could you please clear this up for me.

I don't mean to speak for him but just putting in my 2 cents from experience. Retired PD.

It means what he said, you are capped at $25,000 which is 10% of the 250,000 and the + means you are on the hook / responsible for the additional 10% of what ever that + is.

"... peace of mind ..."

I have live in VA and I use USlawshield/ Texaslawshield. I haven't had to use it but it's a huge relief knowing I have it. You can add your spouse and children in the home for extra fees also includes all 50 states for a small extra fee, also has that coverage as well for an extra option. I bought my year of coverage which is actually 14 months but I had not heard of the class action suit against them. I may have to switch to USCCA when my coverage expires unless they somehow redeem themselves.

USCCA is no longer available in Washington State. They informed me of this last month. It ended in the middle of March. This sucks, as I am a lifetime member. I am looking for a replacement for myself til I get moved out of Washington State in a couple of years.

I read up on this for way too long. I compared the cheapest plans from six companies and like these two best:

1. CCW Safe for the best value and a few more features:

- $149/year for “ccw and police/military, active/retired”; $179 same for “ccw-only”

-- scroll down: https://ccwsafe.com/permit-plans.

- Only company to include spouse and children under 18 when defending themselves inside your house (NRA Carry Guard covers spouse); additional fee for others.

- Only company to cover all of bail bond, up to $500,000. Others pay only the “premium” to the bond (Court may require collateral to cover remainder), generally, 10%, up to:

-- $25,000 for both Armed Citizens (LDN), and NRA Carry Guard,

-- $2,500 for USCCA; $5,000 for Second Call Defense,

-- US Law Shield does not cover bail.

- Only this company and US Law Shield offer “No Limit” on both criminal and civil defense.

-- No limit - criminal / No limit - civil for CCW Safe, and US Law Shield,

-- $50,000 - criminal / $500,000 - civil for Second Call Defense,

-- $50,000 - criminal / $250,000 - civil for both NRA Carry Guard, and USCCA,

-- initial $25,000* – criminal / initial $25,000* – civil for Armed Citizens (LDN).

*after this limit, their board reviews case and allows more if there is “reasonable self-defense”

(see next below)

- Only company to specifically state they cover appeals, expungements, and have a “critical response team come to your location” for booking, etc.

2. Armed Citizens (LDN) for the best value and educational materials:

- $135 first year, $95 year thereafter

- DVDs, textbook, etc. These journals are free, 12/year going back 10 years: https://armedcitizensnetwork.org/en/our-journal

- *the $25,000/$25,000 plan seems reasonable. I can’t confirm, but their policy may be to spend up to $400,000. All insurers will stop payment as soon as defendant “pleads guilty” or there is a conviction. Armed Citizen appears to be checking mid-way to see if you have a chance of being innocent. NRA writes, “Be wary of any provider that claims to offer full criminal defense coverage funding up front: not only is this unnecessary, but such policies would be void in the event of a conviction. Most criminal defense attorneys will not require payment of final bill until after your case ends—at which time the rest of your criminal defense protection is available if you were acquitted or the case was dismissed.”

- Armed Citizen writes their members wanted bail bond protection (second best in this group) more than the extras provided by other companies (expert witness, firearm loss or confiscation during trial, compensation while in court, clean-up of house, psychological support). Their second year and beyond price is $95, much lower than CCW Safe price of $179 for ccw-only customers ($145 for ex-military/police).

NRA carry guard, from what I have read, is no longer available.

USCCA all day. The value is just there, plus they’re classier than the NRA Carry Guard jerks IMO. Seriously, although I do support the NRA, they’re late comers and we’re so rude to the USCCA it was ludicrous.

Noobs to CC should check out the USCCA’s “Into the Fray” videos for sound training . Available on YouTube for free.

Yes if you join you’ll get a lot of email but an unsubscribe can fix that.

The NRA concealed carry insurance program in NY was shut down by the insurance department for various violations and the people selling it had to pay millions of dollars in fines.

Hello, does USCCA cover members excursively when in the United States, or does their member coverage stretch into Canada/Europe.

Thank you

I don't know for sure, but with all the legal issues that would be involved with that, I would bet NO.

I have some experience in the insurance industry and I know a number of people with long experience in the insurance industry. The general attitude of people that have been licensed to sell insurance could be characterized as "suspicion." They wonder what this insurance covers that would not be covered by other general liability insurance such as an umbrella liability policy. Here are some points to consider:

The company itself

Where is the company located? Are they located in one of the states that is tightly regulated, such as New York or California? Are they located in your state?

There are good reasons to ask these questions. One is that they may not be able to pay their claims, or may simply refuse to pay their claims. If they refuse to pay your claim and they are 1,500 miles away with no regulator in your area that you can call on for help, what are you going to do?

It is a good rule that you are far better off buying insurance from large, well-known companies that are registered with the insurance department to do business in your state.

What does it cover?

Criminal costs -- Insurance policies, by law, cannot provide coverage to pay your criminal defense attorney if you happen to commit a crime. The reasons should be obvious -- crime should not be rewarded. Therefore, if any company did guarantee to cover your criminal defense attorney, the only way they could legally do so is after you have been proven innocent. So, if you go to a jury trial, expect to pay for it yourself, whatever.

Civil Liability -- These are payments to the person you injured. Assuming it was a good shoot, a regular liability policy should cover the claim. A CCW would provide no real benefit in this case unless perhaps the settlement went over your policy limits. Your homeowners insurance would probably be primary and the CCW policy would then only pay if your homeowners was maxed out. If that is your worry, then it is cheaper to increase the limits on your existing policy.

What about the exclusions?

If you haven't read the exclusions, and don't want to read them and understand them, then just send me your money for nothing right now and be done with it. The exclusions describe what they will NOT pay. That could be just about everything, or everything, depending on the situation. Discuss it with an experienced claims adjuster or attorney, because simple legal terms have big meanings. Turns out that most insurance policies exclude payments for "intentional acts". Talk to an attorney about whether shooting someone is an "intentional act" that would not be covered. The attorney may not be sure himself.

Also remember that insurance policies are a "contract of adhesion". In legal terms, that means that you have no real right to negotiate the wording. Therefore, if there is any ambiguity in the wording, it will be ruled against the person who wrote the contract -- the insurance company. Therefore, exclusions are written with pretty solid legal language. Ignore them at your own peril.

What's the price?

The prices I have seen for CCW are about in the same range as what you would pay for an umbrella general liability policy with a million dollar limit that would cover you for all liability, not just liability arising out of a CCW incident. That is, you could get a lot more insurance coverage for the same money.

Would I sell CCW insurance?

When I first saw it, I did the math and figured out very quickly that, for the price, coverage, and risk of a claim, this is a better deal for the insurance company than travel insurance. Travel insurance is practically all profit. You collect the same money that the insurance companies get for a policy with much, much broader coverage, the number of claims should be somewhere around "tiny", the insured has to prove he is innocent before they pay anything, and he is in another state so his complaints about not getting paid go nowhere when he finally gets through with his jury trial.

Mathematically speaking, it is a money machine. If I didn't have to worry about getting busted and losing my license for selling it, I would open the insurance company myself.

It should be noted that the state of NY has shut down the NRA CCW program. In addition, the underwriters and agents on that program (all big companies) have agreed to pay millions of dollars in penalties. While the NRA complains that it is about gun rights, it isn't really. It's about questionable insurance products bordering on fraud. Anyone with experience in the insurance laws and any knowledge of how rates are set and claims are paid will tell you right away that there is something wrong with this picture. That's why the agents of the NRA program wound up agreeing to pay millions in fines.

What's the odds of a CCW incident in your life?

One fairly large online survey I saw said that the number of CCW holders who ever actually had to pull their weapon (not use it, just pull it) was somewhere around 2 percent, over their entire lives.

Your mileage may vary. But I wouldn't buy any of them. I would get an umbrella liability policy over and above my auto and homeowners from a reliable company that I know will pay their claims for about the same money.

tl;dr

I thought the same thing. I have a $1 million personal liability with my homeowner's insurance policy, and think I will simply stick with that.

Better make sure that your homeowner's liability policy covers intentional acts. Most insurance only covers accidental, unforeseeable events and excludes intentional acts (like using a weapon in self defense). I'm not saying that you are wrong, I'm only saying this could be a problem and it would be better to find out before you need it.

Im a big fan of your site and really learned much in the past year of subscribing. Thank you.

After much research I chose Self-Defense Fund.

Straight up legal help to just get me put of trouble. No gun give aways or free crap. I could buy what I want with the money saved.

Any thoughts?

Hi Bert, we're going to be slowly adding more. The next up is CCW Safe. It takes a while since we do research and buy the coverage ourselves. But thanks for the rec!

I went with ACLN for the wrong reason, It was the lowest yearly coast. I understand about the emails!. I just open the web site and they started. They offered so much guns and many other things. I finally unsubscribed. I did buy there Concealed Carry magazine, It comes 4 times a year and it is a glossy quality magazine. I enjoy your articles on handguns and accessories I have a save folder for the ones I want to keep. The ones about ARs, precision rifles, and Tactical shotguns, I usually delete them!

The silver plan still exists. However, the gold plan is better for $2 more a month. However, the spouse plan increased from $47 to $147 dollars a year on the annual elite plan. You cannot obtain any more discounts other than this. Personally, I think this is unfortunate. The only other discount is a 10% discount for having served in law enforcement, govt service or military.

Thanks for that info on the spouse plan...I'll reconfirm and update.

Luke, that is incorrect. To add a spouse onto silver is not possible, Gold is $7mo or $77/year, Platinum is $9/mo or $97/year, and Elite is $13/mo or $147/year

Does USCCA no longer offer the Silver plan?

It's a legacy one I believe.

I had it for a year, but dropped it. I was tired of getting my email bombarded by USCCA trying to sell more stuff. I was getting multiple emails for day. It was truly annoying.

The characterization of the coverage under the NRA Carry Guard is really not accurate. I've read the policy and it does not say there is no coverage if you are found or plead guilty. It just says that is where the obligation to pay for or reimburse defense costs ends. The policy covers everything (up to policy limits) up to the end of the case (but not including appeals). You say that the lack of coverage is a BIGGIE and its not accurate. This article really needs to be edited to fix this. Policies are complicated and discussing coverage when you don't have a law degree is, even with a disclaimer, not really doing folks a service. Please consider editing the article to be more accurate.

I don't know anything about insurance, but I do know business. I know enough that anything not spelled out in writing is something you will never see.

If the NRA policy says "that's where our obligation ends", I can promise you....THAT is where their obligation will end.

It would foolish to assume that if you are found guilty that the NRA is going to pay out the other 80% just because they think you're an "ok guy"

That goes double with insurance. Count on it. Anything that is ambiguous in an insurance policy is construed against the company. Therefore, they pay for anything they didn't say clearly. They cast those words in iron.

The state of NY has shut down the NRA program, at least in their state, and the underwriters and agents who were selling it have agreed to pay millions in penalties for violating various insurance laws and selling dubious policies. There are fundamental problems with the idea of offering CCW insurance in the first place.

The unfortunate thing is at the end of the post appears to be your disclaimer...

You close your post disclosing you provide video content for USCCA. This is where you seem to lose credibility as you state you provide video content for USCCA after membership purchase...

Please explain...

Hey Mark, great question. USCCA reached out after my unsolicited review and saw that Pew Pew Tactical offers a beginner gun course (created for our readers who wanted to get a beginner/refresher course on handgun safety). They thought it would be a great idea to cover the cost of the course for people.

Maybe they should send them to thier own certified insurance salesmen er firearm instructors!

I have been a Life Member of the NRA for over 20 years. I belong to USCCA for several years. I was under the impression that my spouse ( domestic partner) would need a separate full member ship. We both carry and have been together over 6+ years. When I contacted USCCA to upgrade, I was informed of my new cost per month. When asking about my partner I was told her membership would be covered for a small one time fee per year and I would receive a senior discount off the reg. cost.

Whenever I call they are very friendly, knowledgeable and have all my answers. I would never change to Carry Guard or any other program. In addition the web site is user friendly and easy to navigate.

Jerry

Eric, Great article but has anyone actually analyzed the avg cost of a "case" when someone is a shooter? I purchased the Platinum coverage and even called USCCA to ask them what was the cost of the "average case" when I was deciding. CS reps said they did not know but sure that someone at USCCA does as this is how the monthly/annual rate is set. CS Reps offered to give me some lawyers in the area to ask this question. Don't get me wrong as I think USCCA has lots of benefits to offer but I also would love to see the numbers. Your link to "cost" does not really cover cost so one could do a Cost-Benefit-Analysis against the risk. This is what USCCA has up on their web page: https://www.usconcealedcarry.com/the-cost-of-defense/

Hey Eric, I'm not super sure of the "average case" cost either since there are so many factors...location, lawyer choice, booking, etc.

Just to understand , you have to bond yourself self out of jail and pay a retainer to an attorney. Basically, the same things in dealing with the courts now.

Unfortunate that USCCA does not offer memberships in NRA. At least offer as an additional/

Eric, great job as always!

I’m a member of both organizations. We use USCCA for CCW coverage and NRA for Instructor coverage. I wish USCCA would provide that as well, NRA quite frankly is pretty lame. I’ve received varied answers to coverage questions and they really danced around with answers to others.

I'm a USCCA Platinum member, Went with Texas Law Shield my first year, being from Texas & their plan's not bad. But after reviewing other insurers I switched to USCCA when it was time to renew my Texas Law Shield protection. I think it's the best deal out there, also. JMO. Hope I never have to use it.

You only give out the free lessons to FULL YEAR payor? Or do I at least get that access after paying all year on monthly?

Thank you Eric,

I have been very pleased with USCCA since 2011, they have been pleasant to deal with. I do not see me changing ins at all, the magazines are of high quality from the beginning. I do have my wife added, I signed up after hearing about the company during our first visit to Pahrump, NV.

PS I did hear the Law Schield people speak in about 2015 and they were nice folks, they made their coverage sound interesting.

Very helpful article and information. Thought I would add to the discussion by including a link to a page that compares the top five companies. USSCA is the final column titled "Other Insurance Product. https://ccwsafe.com/page/quick-comparison-of-service

Eric:

In the USCCA fine print located at https://www.usccacoverageform.com/, it states in:

Section 1 – Coverages,

1.. Insuring Agreement,

b. (2) Our right and duty to defend ends:

(b) With the insured’s “conviction” of any criminal charge(s)

So, it appears, like the NRA coverage, they stop paying for any services once a guilty conviction is arrived at. Thoughts?

Hey Jim, not a lawyer, but looks like it. Though at that point it might be the least of your worries!

Thank you so much for this article. I'd be curious how those two listed compared to US Lawshield. I purchased US Lawshield insurance at the end of an IL CCW class when a rep came in to tell us all about their program. It was only $131.40 per year. I don't know if "you get what you pay for" holds true for this instance. US Lawshield didn't send me anything in the mail. The only thing I have to show that I'm covered is a card that was included in the sign-up flier. Their member portal is REALLY weak. I don't know; I think I may have gotten the wrong insurance for this year. I'm wondering if anybody who reads this has dealt with US Lawshield.

Thanks for sharing your experience, hopefully others will chime in too!

Splendor,

I do remember signing up with LS in about '14 or '15. Somehow my first payment got messed up and could never get it fixed, Your word weak does come to mind, I never could make a break through so I just stopped working on it and realized that USCCA was where I needed to stay.

Seems that I remember that they press their members into service on building membership, may be that customer service is the same thing and not enough training and experience?

I did get a nice double folder the day that I signed up with all sorts of info, I do not know if I got anything in the mail from them.

Eric, I edited to add some info about Law Shield and cannot get it to repost. Can you help?

I was working on an EPL membership, paying my quarterly $25 payments every three months. I got on my computer to make my next payment. My account on their website said I had a yearly membership, however on my previous payments my account clearly said EPL. I sent three e-mails, each about a week apart, asking them to fix the problem. I never heard back from them. The first e-mail was polite, the next two were i increasingly angry. After the third e-mail was sent, I checked to see if my status was fixed. Not only was it not fixed, my account was deleted. so this is how they handle there own screw ups.

When the NRA bumped me down to yearly, my magazine subscription went from EPL to expiring a year and a half down the road. I gave up on these incompetent idiots after the third e-mail. A few months later I got to thinking about how they screwed me out of the EPL membership, I got mad all over again, I checked my e-mail to see if I got a response from them. Not one word. So I sent them an actual letter along with my membership card telling them what they can do with it and to never send any more literature whining for more money for a membership or for any other reason. My magazine subscription stopped 15 months earlier than what the printed address label on my latest magazine stated.

They are constantly soliciting for memberships and donations so that they can continue the fight and they pull garbage like this. How are they going to continue if they keep screwing people over? I know I can't be the only one.

If I could give zero stars to the NRA, I would. They certainly don't deserve even one star.

Interesting and great reaffirming article! I “had” the NRA Carry Guard insurance, however after the recent “fleeing” of certain companies from the NRA (including the underwriters for the Carry Guard insurance, Chubb) I am now a member of USCCA and couldn’t be happier, especially with the main points you highlighted in the article. Had a very close friend of mine get into the financial train wreck of having to deal with a self defense situation and he had and will continue to carry USCCA, he stated if it weren’t for them he would essentially be homeless right now.

NRA Member and I have the NRA carry guard insurance, but recent NYS Attorney General issue voided the insurance in NY State and at expiration the underwriter will not renew in NY State. Any comments about this would be appreciated. Does the NY State insurance rule apply to USCCA as well?

Well,does nys rule also apply to other ins.?

Uscca?

I'd like a definitive answer to this as well; I used to have a USCCA policy that was ended at the end of June (I got a lot of notifications about the DFS decision), but it looks like it's available again to join from my account. I keep asking different instructors and others from USCCA but noone seems to be able to tell me for sure that the NYS DFS situations was rectified, and if so, how? The 'complete coverage form' appears dated at the end of June which would suggest it was modified to correct those issues as it spells out clearly that payment is not made for claims found to arise out of a criminal act on the part of the insured. But given the situation this year, why is there no FAQ on their site that's like 'Yes, the policy is now NY-compliant'?

Eric: GREAT Article. I was a Gold Member but I upgraded to Platinum, after reading this article. Also, I had Insurance coverage on my gun collection with NRA this past year. When my renewal was up, I found another carrier, Collectors Insurance. Their coverage is better and their cost was about half. You should write an article on that comparison as well.

I researched them all and I've been with CCW Safe for 5 years. I think they have the best coverage and are the best value in the industry. I highly recommend looking into their coverage/price if you looking for protection. I'm not associated with them, just a satisfied member.

Sounds like this was written by some top salesperson for the company. Sorry, that's just my opinion.

This kinda sounds like it was written by the competition. Just kidding!

But no, it's by me who did some research before settling with USCCA. And I'm still paying every month for my coverage just like anyone else.

Just signed up for the hold plan, thanks for the article better safe then sorry

Glad we could help, Lori!

Why did you settle with them and not an umbrella policy on your insurance?

CCW.

pretty good imho.

Thanks Brad!

Your the best, Eric. How do you always know what I want to know LOL. Seriously though, thank you!

You're so welcome, and...I try LOL

Not available in New York ??????????

I have a question and look for any info others can provide. I currently have the NRA Carry Guard (it renews this month) and I looked over the USCCA policy and information about it and found it had many things I liked that are not in the NRA policy. Early in the USCCA policy there is reference to terms on the Declaration page (for example, the Each Claim Retention Amount) that are not fully explained or defined in the body of the USCCA policy. I called USCCA and asked to see a copy of the USCCA policy Declaration page and was told they would not provide me with a copy of the policy. The representative with whom I spoke was nice enough but I don't think he really understood the reason I was asking for a copy of the Declaration page but was just reading from a script or canned answers. I was the General Counsel for an international property & casualty insurance company for close to 30 years and know that important information is on the Declaration page. Has anyone encountered this issue and been able to work through it with USCCA (or gotten a satisfactory answer as to why you can not see the Declaration page)? Thanks